Klarna (NYSE: KLAR) — Confidence Signals, Channel Optics, and the Economics Beneath the Story

Author’s Note: We may from time to time hold long or short positions in Klarna securities, including stock, debt, or derivatives associated with the stock, and therefore may have an economic interest in changes in Klarna’s market price. The information presented in this report is derived from public records and other publicly available sources. Sources are listed at the end of this report. Readers should review those materials and draw their own conclusions.

Executive Summary

1) A board-chair “confidence buy” was promoted into a lock‑up microstructure event—at precisely the moment the market was anxious about supply. In early March 2026, Klarna unusually publicly “clarified” that the March 9 lock‑up expiration did not mean insiders could immediately sell, emphasizing a transfer‑agent conversion process (including a “Letter of Transmittal”) that it said would take ~7–10 business days at minimum. Shortly thereafter, Klarna issued (and syndicated) a press release highlighting that Michael Moritz—through an associated nontaxable entity—had purchased 3,472,845 shares for $49.9M (March 3–11) and tied the disclosure to the related SEC ownership filing. The filing itself shows the stake was held indirectly through Crankstart Foundation and provides the purchase window and price range.

Why it matters: in securities‑law terms, the risk is less about “illegality”; it is a credibility tax—the perception that the issuer is managing optics (float, supply, insider alignment) at a moment of elevated sensitivity. In activist terms, it is a tell: the company may have believed the lock‑up narrative itself was price‑relevant enough to warrant proactive “mechanics” coaching.

Strongest counterpoint / uncertainty: open‑market buying by a board chair can be authentically bullish; the company’s release also disclosed smaller insider sales (including noting they were under 10b5‑1 plans), which cuts against a simplistic “pump” framing.

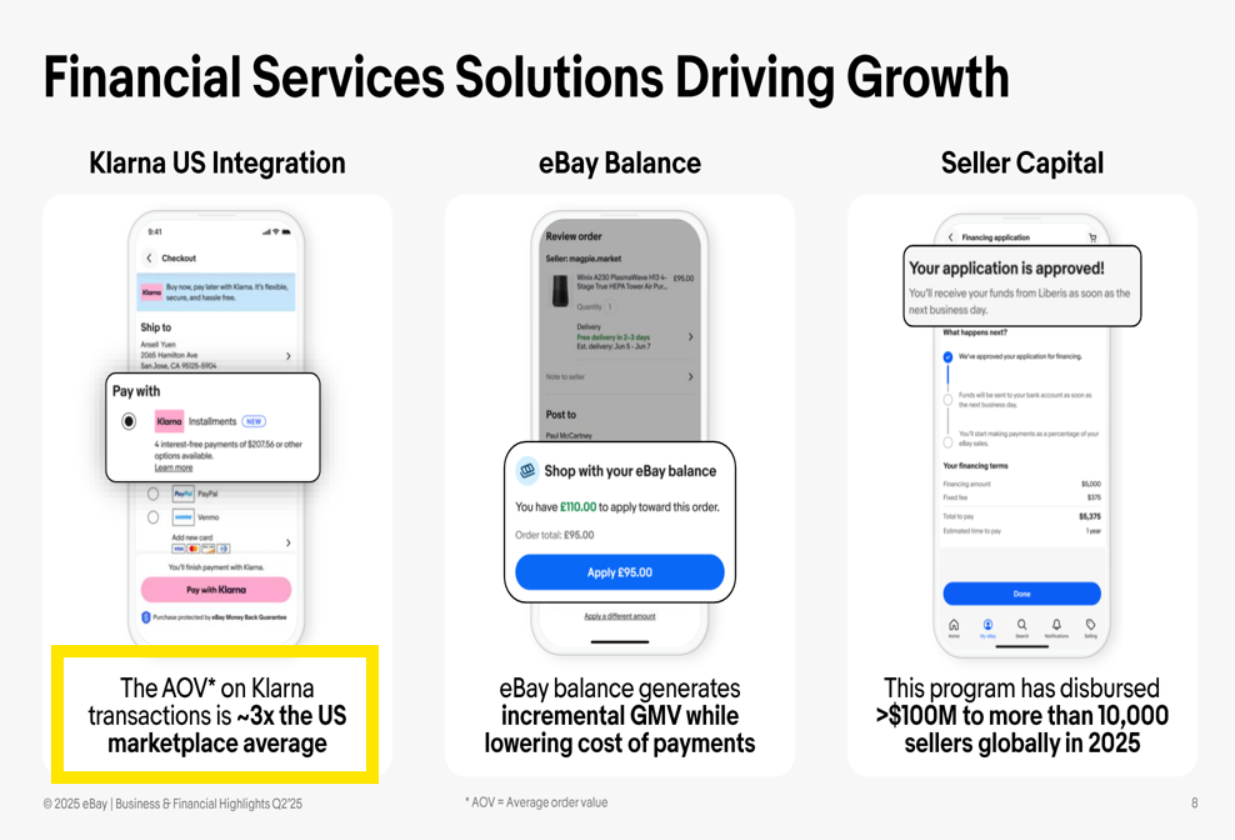

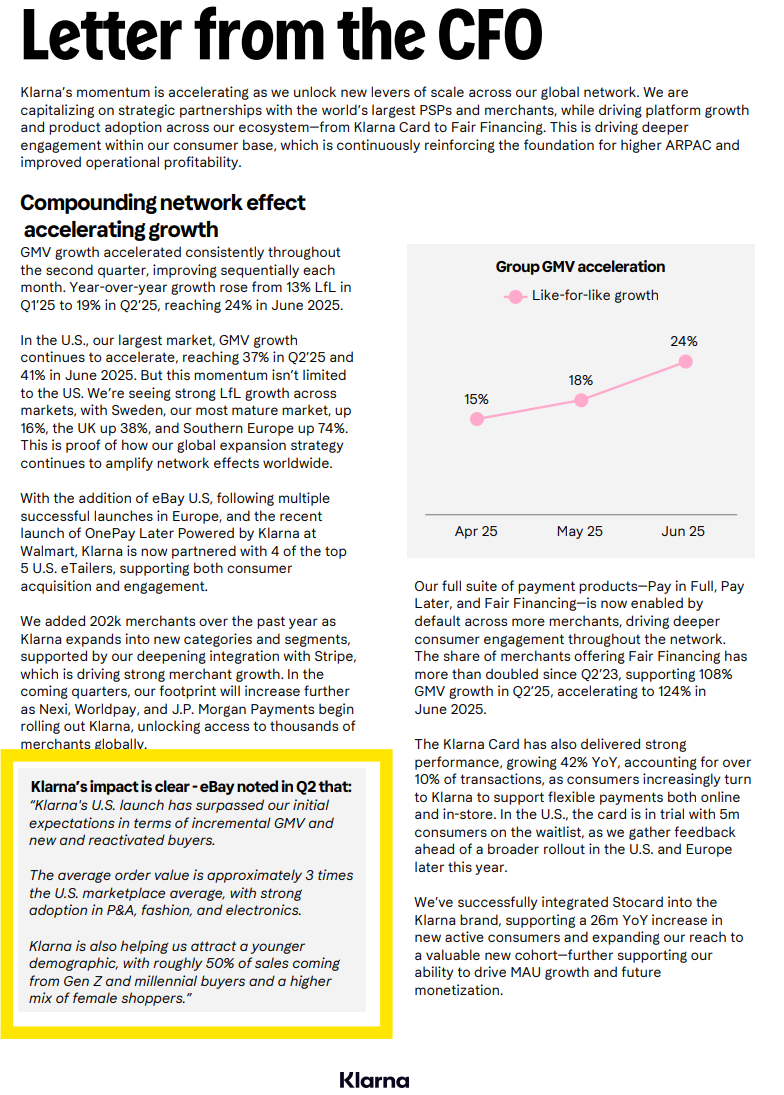

2) The eBay “~3×” uplift story appears materially entangled with eBay‑funded, threshold‑based couponing—exactly the kind of mechanism that inflates basket size and produces headline metrics that may not survive normalization. In eBay’s Q2 2025 earnings presentation, the company stated: “The AOV on Klarna transactions is ~3× the US marketplace average.” Klarna then amplified a similar framing in its own Q2 2025 earnings materials, quoting eBay that the U.S. launch was driving incremental GMV, and repeating the “~3×” AOV claim.

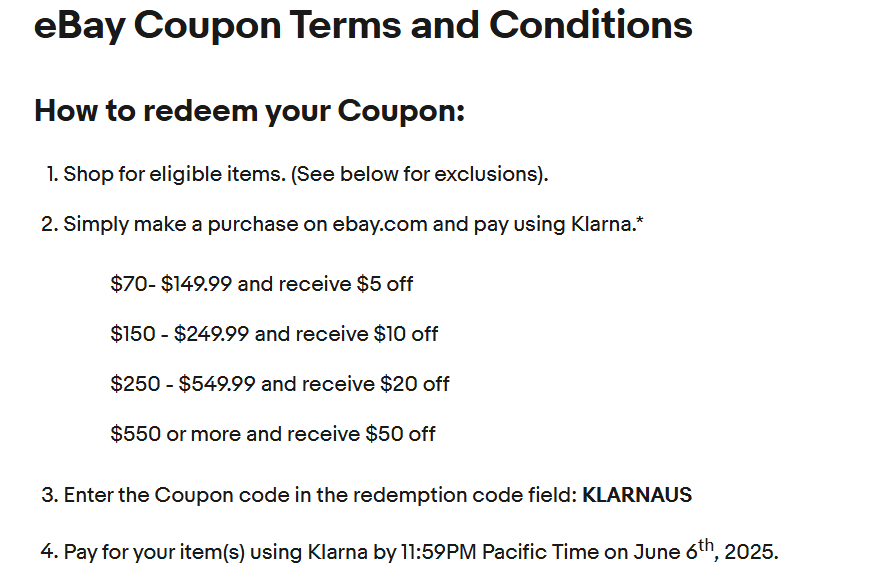

But eBay simultaneously ran a time‑boxed U.S. promotion requiring Klarna as the sole payment method, with tier thresholds around basket sizes of $70 / $150 / $250 / $550 designed to pay escalating discounts (up to $50) and expressly stating: “Coupon is funded by eBay,” valid June 2–6, 2025—within the Q2 reporting period.

Why it matters: promotions are not “wrong.” The issue is whether investors are being led to treat a promotion‑accelerated metric as evidence of durable Klarna-driven uplift. Where the mechanism encourages shoppers to “round-up” their carts to thresholds, the form of the statistic becomes suspect.

Strongest counterpoint / uncertainty: AOV differentials can also be a true selection effect (BNPL used disproportionately for higher‑ticket categories). The record does not prove the coupon drove most of the 3× statistic; it shows a serious, quantifiable confounder that should have been made explicit where the claim is used as evidence of intrinsic lift.

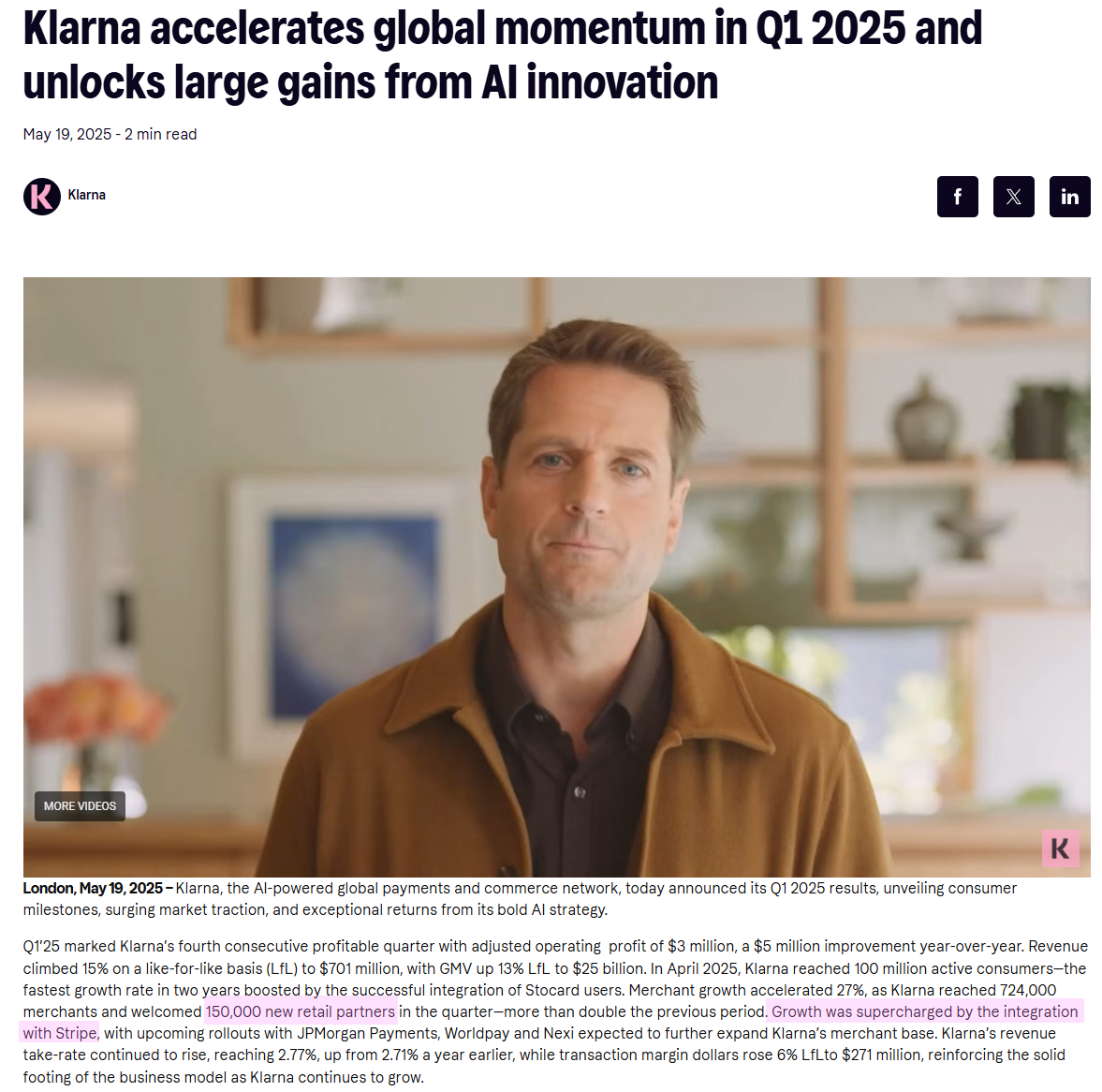

3) Klarna’s Stripe “distribution flywheel” is also a concentration and measurement problem—especially around the IPO narrative. Klarna strengthened its partnership with Stripe so that Stripe‑powered businesses in 25 countries could “instantly” offer Klarna, and Klarna stated this helped it double the number of new merchants offering Klarna for the first time in Q4 2024. By Q1 2025, Klarna claimed it reached 724,000 merchants and “welcomed 150,000 new retail partners,” explicitly attributing acceleration to the Stripe integration, with additional PSP rollouts pending.

Klarna’s own FY2025 annual report language is unusually candid that it derives a “substantial portion” of merchant revenue from merchants using “merchant of record” PSP channels, naming Adyen and Stripe, and stating it plans to continue driving GMV and revenue through those channels.

Why it matters: this is the double‑edged sword of embedded distribution. It can accelerate “merchant count” and enablement—but also creates bargaining power for the platforms and creates metric‑quality questions (“enabled” vs “active”; gross adds vs churn; who is being counted).

Strongest counterpoint / uncertainty: Klarna is not hiding the channel strategy; it discloses it. The open question is whether public‑market investors are correctly discounting the difference between “distribution‑enabled” growth optics and durable, direct merchant pull.

4) The earnings narrative depends heavily on non‑IFRS framing and on the timing/price of receivables sales—both of which can obscure stress until it is no longer containable. Klarna’s Q4 2025 materials emphasize “Transaction margin dollars,” “Adjusted operating profit,” and like‑for‑like growth as key management measures. The same Q4 package discloses significant receivables offloading and a gain on sale (and, separately, accounting losses when selling certain consumer receivables while retaining merchant fees).

Why it matters: for a credit‑intermediating fintech repositioning as a “digital bank,” cost of capital and credibility can turn on whether reported profitability is repeatable absent favorable securitization/forward‑flow pricing—and whether credit costs are being “explained away” as temporary timing effects.

Strongest counterpoint / uncertainty: IFRS loss provisioning mechanics are real; some margin compression can be timing‑driven during rapid growth. The bearish implication depends on whether credit and funding normalize benignly—something the public record does not yet conclusively resolve.

5) Klarna’s recycled-phone-number login issue raises a more basic question of trust: whether controls around identity verification and customer-data access lagged the company’s growth and conversion priorities. Business Insider reported that internal Klarna messages initially modeled a theoretical exposure of up to 288,000 customer logins and a potential $41.8 million legal/remediation cost tied to insufficient protection against recycled mobile numbers, before Klarna later said actual impacted accounts were more than 99% lower than that initial theoretical scope. The attached Reddit complaint is directionally consistent with the same failure mode: a user alleged that OTP access tied to a recycled phone number exposed another customer’s full name, date of birth, email address, cards on file, and billing address. The lasting issue is not whether the highest internal estimate proved overstated; it is that a consumer-finance platform appears to have allowed authentication design, escalation, and control hardening to remain vulnerable until a public incident forced broader remediation. Klarna says the issue affected only a very small subset and has since been resolved.

Bottom line: The short thesis is not that Klarna lacks scale. It is that Klarna’s public‑market narrative increasingly relies on (i) confidence signaling around supply moments, (ii) partner‑ and promotion‑inflated “impact” metrics, and (iii) distribution channels that drive optics faster than they prove durable economics—while (iv) earnings quality remains unusually sensitive to credit mix and receivables‑sale pricing.

Best bull case / counter‑catalysts: Klarna’s defenders will argue this is exactly how platform distribution works (Stripe enablement is real distribution, not “optics”), promotions are ordinary acquisition spend, and Moritz’s buy is a straightforward (ignoring nontaxed entity selection) alignment signal. If credit metrics remain stable and receivables sales stay available on attractive terms, the equity can re‑rate from a depressed base.

Why This Matters Now

Klarna is living through a classic post‑IPO arc: the business tries to widen its identity from “BNPL” to “bank,” while the stock’s reality is more of a leveraged bet on consumer credit quality and funding. That is not an insult; it is capital structure reality. The market’s job is to decide whether the issuer’s growth is high‑quality—driven by durable consumer and merchant preference—or whether it is assisted by transient mechanisms: partner distribution, promotions, and securitization/forward‑flow timing.

The March 2026 lock‑up sequence is why this story is acute now. The company affirmatively instructed investors not to over‑interpret the lock‑up date, emphasizing conversion process delays and the fact that large blocks were not instantly transferable, due to processing through Computershare. Immediately thereafter, the company highlighted a $50M chair‑linked purchase. This is exactly the kind of “microstructure + messaging” cocktail that, in other issuers, frequently precedes volatility: the issuer is implicitly conceding that supply expectations can move price.

At the same time, the regulatory disclosure perimeter for foreign private issuers tightened and continues to be an investigation and enforcement priority for The U.S. Securities and Exchange Commission (“SEC”). The SEC announced final rules implementing the Holding Foreign Insiders Accountable Act, extending Section 16(a) reporting to directors and officers of Exchange Act‑reporting foreign private issuers, with effectiveness tied to March 18, 2026. That change increases visibility into insider‑aligned trading activity—precisely when lock‑ups roll and promotional narratives matter most.

Against that backdrop, the quality of “partnership economics” becomes crucial. eBay’s “~3× AOV” framing is illustrative: it is a powerful headline, but it sits adjacent to a structured, eBay‑funded coupon with tier thresholds that mechanically encourage larger baskets—an example of how partnership marketing can outrun normalized economic substance. The recently expanded Klarna-Stripe partnership belongs in the same analytical frame: if a closely related intermediary can catalyze a step-change in merchant adds, headline adoption may say as much about sponsor-adjacent distribution support as about normalized, arms-length demand—especially given Sequoia Capital’s significant Stripe ownership and board representation. The market does not need perfection; it needs candor. Where candor weakens, discount rates rise.

Company and Situation Overview

Klarna presents itself as a scaled payments network converting consumer relationships into broader financial services. Its annual report frames merchant relationships and consumer engagement as the backbone of its economics, with revenue heavily tied to merchant activity and transaction volume.

Two strategic choices define the current setup.

First, Klarna has decided to scale distribution through large payment‑service providers and “merchant of record” partners. In its own description, PSPs—including Adyen and Stripe—can sit between Klarna and the underlying merchant, allowing Klarna to “reach and bring” a substantial number of merchants onto its network. The same disclosure states Klarna currently derives a “substantial portion” of merchant revenue from merchants using those MoR channels, and intends to continue driving GMV and revenue through them. This is not a footnote. It is Klarna’s central distribution strategy.

Second, Klarna’s financial narrative depends on how it contains credit and funds receivables as it expands higher‑frequency or longer‑duration products. Its Q4 2025 disclosures emphasize non‑IFRS performance measures (including “Transaction margin dollars” and “Adjusted operating profit”) and discuss receivables offloading and gain‑on‑sale dynamics as part of capital‑efficient growth. In a benign environment, that can be a genuine ROE enhancer. In a stressed environment, it becomes the first place investors ask: what is true earnings power without favorable asset‑sale pricing?

This matters because the market has already signaled sensitivity. Reporting and market commentary around February 2026 reflected sharp negative reaction to credit provisioning and losses, even as revenue grew—an archetypal “growth vs credit quality” trade‑off response.

Key Chronology

· December 2020: Klarna announced that Michael Moritz would assume chairmanship of the board (having served on the board since earlier investment involvement).

· January 2025: Klarna announced a strengthened distribution partnership with Stripe enabling Stripe‑powered businesses in 25 countries to “instantly” offer Klarna; Klarna said this doubled new‑merchant adoption (Q4 2024 vs prior quarters).

· May 2025 (Q1 results): Klarna stated it reached 724,000 merchants and “welcomed 150,000 new retail partners,” attributing acceleration to the Stripe integration and highlighting future PSP rollouts.

· June 2–6, 2025: eBay ran a U.S. coupon requiring Klarna as sole payment method with tiered discounts at $70 / $150 / $250 / $550 spend thresholds, noting the discounts were solely funded by eBay.

· July 30, 2025: eBay’s Q2 2025 earnings presentation reported that AOV on Klarna transactions was ~3× the U.S. marketplace average.

· September 9–11, 2025: Klarna priced and closed its IPO at $40/share; shares began trading on the New York Stock Exchange under ticker KLAR; a majority of the IPO shares were sold by selling shareholders rather than the company (similar to another recent Sequoia-linked IPO we’ve written about: Figma).

· February 19, 2026: Klarna released Q4 2025 results materials emphasizing non‑IFRS measures and discussing receivables sales/offloading dynamics.

· February 27, 2026: The SEC announced final rules implementing the Holding Foreign Insiders Accountable Act and extending Section 16(a) reporting to directors and officers of Exchange Act‑reporting foreign private issuers (effective March 18, 2026).

· March 6, 2026: Klarna issued a press release clarifying March 9 lock‑up expiration mechanics, including a conversion process via Computershare and an indicated 7–10 business day minimum processing time after receipt of a completed Letter of Transmittal.

· March 3–11, 2026 / March 12 filing: Moritz‑linked buying occurred in that window and was disclosed via Form 3 filed March 12.

· March 13, 2026: Klarna publicly circulated a press release highlighting the chair’s purchase (and disclosing other insider buys/sells).

Core Analysis

Issue one: the company chose to “teach the tape” on lock‑up mechanics—then highlighted a chair‑linked buy. The legal risk is not a clean claim of wrongdoing; it is the appearance of a managed market narrative at a moment of maximum sensitivity.

Lock‑ups are ordinary. What is unusual here is the issuer’s decision to publish a granular, quantitative “mechanics” note designed to rebut a specific market interpretation of the lock‑up date. Klarna stated that before certain shares could be sold through U.S. broker‑dealers (other than its transfer agent), holders would need to complete a conversion process administered by Computershare, with a minimum processing time of “approximately 7 to 10 business days” after receipt of a completed Letter of Transmittal. It further broke down how many shares had not initiated the process and how many holders had elected conversion choices that preserved voting rights.

On its face, the release is framed as investor education. But investor education is not value‑neutral when it is deployed in response to “coverage suggesting” that insiders could sell immediately. It is, implicitly, a defense of price stability. The market does not reward issuers for explaining settlement mechanics unless people are worried about supply. The more important point is that Klarna’s disclosure choices show management believed that the perceived tradable float—not merely the underlying business—was a near‑term driver of valuation.

Within the same short window, Klarna highlighted that the chair, Moritz, “through an associated entity,” purchased 3,472,845 shares for $49.9 million, and the Form 3 filing specifies those purchases were executed via open-market purchases from March 3–11 at prices ranging from ~$13.18 to ~$16.11. The filing also reflects that the ownership is held indirectly through a non-profit: Crankstart Foundation. Crankstart’s own website identifies its founders as husband-and-wife duo: Harriet Heyman and Michael Moritz. This is a public fact, but important for understanding that this is not an unrelated third‑party buyer.

An activist short seller cares about this for three reasons.

First, the timing creates a foreseeable inference problem. When a company pairs (i) a statement that supply is not immediately coming and (ii) a “confidence buy” headline, the market may interpret the combined message as reassurance. Whether or not that was the intent, it is plausibly the effect. And when optics become part of capital‑markets strategy, future credibility is often the first casualty.

Second, the governance framing is fraught. Moritz is not a random director; Klarna itself announced his chairmanship publicly and has framed his involvement as long‑standing. Chair‑adjacent buying may be perfectly lawful, but it increases the level of scrutiny around information barriers, board processes, and trading pre‑clearance protocols—especially for a company repositioning as a “digital bank” where supervisory expectations on controls are higher.

Third, the disclosure regime is tightening. The SEC’s implementation of the Holding Foreign Insiders Accountable Act extends Section 16(a) reporting to directors and officers of reporting foreign private issuers effective March 18, 2026. That matters because expanded reporting visibility can turn what would otherwise be a “soft” optics issue into a repeatable pattern visible to the market: the cadence of insider buys, sells, 10b5‑1 explanations, and Form 144 filings.

None of this proves wrongdoing. The defensible claim is narrower and more material: Klarna has begun to operate as if its stock price depends on managing supply perceptions and broadcasting endorsement signals. That distinction matters, because once a company crosses that line, skeptics stop treating disclosure as neutral reporting and start treating it as narrative engineering.

Issue two: the eBay “~3×” claim is a case study in promotion‑inflated optics—because the incentive structure was designed to increase basket size, and the issuer‑partner narrative did not contextualize it when citing the statistic as evidence of impact.

Begin with what is not disputed. eBay’s Q2 2025 earnings presentation includes a slide titled “Financial Services Solutions Driving Growth,” and in the “Klarna US Integration” panel it states: “The AOV on Klarna transactions is ~3x the US marketplace average.” Klarna’s own Q2 2025 earnings release then amplifies this framing—quoting eBay that Klarna’s U.S. launch surpassed expectations, was driving incremental GMV and new/reactivated buyers, and that average order value was approximately three times the U.S. marketplace average.

Now read that headline claim against the economic mechanism eBay simultaneously deployed. eBay’s official coupon page during Q2 2025 offered a tiered discount that required Klarna as the sole payment method. The thresholds—$70 minimum spend, with step‑ups at $150, $250, and $550—are not subtle. They are precisely the kind of incentives that cause rational consumers to “top up” carts to reach the next discount. The page expressly states: the coupon is funded by eBay and was valid June 2–6, 2025.

This is the core analytical dispute: Is the “~3× AOV” statistic being used as a claim about Klarna’s intrinsic ability to drive higher‑value purchasing, or is it (at least in part) an artifact of targeted, eBay‑funded promotions that induce basket inflation? The record, as it stands, does not allow a decisive causal proof either way because neither party discloses the underlying distribution. But the existence of the coupon program is not a minor detail, because it is a known confounder embedded directly in the quarter being cited.

There are three ways this can mislead sophisticated investors even absent any formal false statement.

First, it can create selection bias masquerading as product effect. AOV on Klarna transactions can be higher because Klarna users choose the product at checkout for higher‑ticket categories. That is normal. But the coupon thresholds are explicitly correlated with transaction size. If the coupon drove a surge in Klarna‑routed orders near threshold points, the average will rise even if underlying consumer willingness to spend does not change.

Second, it can function as subsidy attribution confusion. The coupon is “funded by eBay.” That is an acquisition cost. Investors who treat AOV uplift as proof of “better customers” might implicitly credit Klarna for a benefit that, in that moment, may have been bought by eBay marketing dollars.

Third, it risks becoming a recyclable talking point. Once a partner metric becomes press‑ready, it tends to be re‑used in subsequent fundraising, merchant pitches, and investor materials. If it is promotion‑sensitive, the market will eventually learn—often abruptly—when the program ends and the metric decays.

The proper way to treat this is neither scandal nor shrug. It is an evidentiary demand: if Klarna is going to cite this kind of “impact” KPI to support U.S. momentum, it should disclose the role of partner promotions when they are designed to mechanically increase the numerator. In the absence of that candor, investors should apply a discount to partner‑sourced “uplift” narratives.

Click below to expand each image (yellow boxes added for emphasis):

Issue three: Stripe distribution proves reach—but it also proves dependence. The more Klarna’s merchant growth becomes “default‑on” through platforms, the more its merchant metrics look like enablement statistics rather than demand statistics, and the more valuation should treat growth as channel‑mediated.

Klarna’s Stripe relationship is real and powerful. The company’s own press release describes that Stripe‑powered businesses in 25 countries can “instantly” offer Klarna, and it attributes a doubling of new merchants offering Klarna in Q4 2024 to the strengthened partnership. By May 2025, Klarna was publicly attributing merchant growth acceleration to the Stripe integration, claiming 724,000 merchants and 150,000 “new retail partners” in the quarter.

The reason this matters for an activist short report is that the company’s own annual report gives away the key risk framing: Klarna discloses that PSPs including Adyen and Stripe act as “merchant of record” partners, and—most importantly—that Klarna “currently derive[s] a substantial portion of [its] merchant revenue from merchants utilizing” those MoRs, with plans to continue. That is not mere “distribution leverage.” It is a structural economic dependency on large platforms that can influence product placement, pricing dynamics, and integration friction.

This dynamic becomes especially salient around an IPO window because the market tends to reward scale indicators (merchant count, consumer count, GMV acceleration) without always distinguishing enablement from activity.

Klarna’s own materials provide the language an activist would use to pressure‑test this distinction. It discusses becoming a default payment option with PSPs and names partners including JPMorgan Payments, Stripe, Nexi, and Worldpay. It also discloses reliance on third‑party providers and cites Stripe specifically as a distribution partner through which Klarna offers payment methods across Stripe merchants globally. Sequoia Capital’s footprint also runs through both sides of this distribution channel: Sequoia-affiliated funds beneficially owned >20% of Klarna’s voting control post-IPO, while Michael Moritz serves as Klarna’s chair and also sat on Stripe’s board until late-2023 (other Sequoia directors currently sit on both boards); Stripe does not publicly disclose Sequoia’s exact current ownership, but Sequoia’s 2024 LP materials valued its Stripe position at $9.8 billion against a $70 billion 409A valuation, implying an estimated stake of ~14%.

There is a subtle but crucial point here: the merchant metric becomes less informative as “default‑on” distribution expands. If a merchant has Klarna “available” through Stripe but never activates it meaningfully (or activates during a promo window and then goes dormant), counting that merchant in a headline total can overstate economic breadth. This is not a claim that Klarna lies. It is a claim that the market may be over‑reading the metric—and that management has incentives, post‑IPO, to emphasize the most flattering version of the count.

The counterargument is credible: embedded distribution is a legitimate growth strategy; Stripe integration reduces friction; and Klarna has disclosed meaningful partner‑channel reliance. The activist response is equally credible: disclosure is not the same as measurement discipline. If investors are being asked to pay for acceleration, they should demand cohort transparency—GMV per “new merchant,” activation curves by channel, and churn of newly enabled merchants.

Klarna Press Release: Stripe integration “supercharged” growth

Pink highlights added for emphasis.

Issue four: earnings quality is increasingly sensitive to receivables‑sale pricing, credit‑mix shifts, and non‑IFRS framing—so the market should treat “profitability” as contingent, not structural, until proven otherwise.

Klarna’s reporting emphasizes “Transaction margin dollars” and “Adjusted operating profit,” and its Q4 2025 materials provide extensive explanation of non‑IFRS measures and why management views them as the most meaningful indicators of performance. That choice is not inherently problematic. But it is a signal of where management believes investor skepticism is concentrated: transaction costs (processing, credit losses, funding) and the perceived visibility of “true” profitability.

The same disclosures acknowledge that significant receivables sales and offloading programs are part of the model, including the recognition of gain‑on‑sale dynamics and the economic differences between selling different product receivables. For earlier periods, Klarna similarly described major forward‑flow facilities and warehouse capacity, and highlighted deposit growth and a low “cost of funds” statistic expressed as a percent of GMV.

This is where the bearish thesis becomes financially concrete. The market should ask three questions, each of which has direct valuation implications:

First: how much of the reported improvement is driven by repeatable unit economics versus timing and pricing of asset sales? If gain‑on‑sale economics are favorable, earnings can look better. If spreads widen or risk appetite fades, the same activity can compress or reverse. The risk is discontinuity: investors price smooth compounding; structured finance can deliver step‑function volatility.

Second: how robust is the “credit is stable; provisions are timing” narrative? Public commentary around February 2026 emphasized that the stock reacted sharply to higher provisions and losses even as revenue grew, reflecting investor discomfort with the “deferred value creation” story. If the credit product mix continues shifting toward longer‑duration “fair financing” cohorts, the company can remain in a perpetual state of “profitability lag”—unless cohort performance and funding are strong enough to overcome the front‑loaded loss recognition and the economics of loan sales.

Third: are investors being asked to accept “economic” profitability that excludes meaningful recurring costs (share‑based compensation, restructuring, and other excluded items) while the statutory bottom line remains weak? The full‑year 2025 summary presented adjusted operating profit (and margin), but also negative EPS. The distinction matters for valuation because the public market ultimately prices cash‑flow credibility, not adjusted narratives.

A fair reading acknowledges that Klarna is at least disclosing the components and explaining the mechanics. The activist‑short inference is that the margin story is still being proven, and its proof relies on external market conditions (funding and forward‑flow appetite) that can change quickly. That is a fragile foundation for multiples.

Issue five: recycled-phone-number authentication suggests an uncomfortable trade-off between conversion and control integrity.

According to Business Insider, internal Klarna Slack messages described a failure mode in which a newly assigned mobile number could, in some cases, be used to access the prior owner’s Klarna account and view personal details. BI further reported that similar incidents appeared in support records dating back at least to 2022. Klarna’s public position was narrower: it said this was not a system-wide breach, that the initial 288,000 figure was only a starting point for investigation, and that the actual impacted population was more than 99% below that initial theoretical scope. Even on that narrower framing, however, the issue is serious because it goes to identity verification at the point where a payments and credit platform is handling sensitive consumer data.

What makes the episode especially relevant for investors is the governance implication embedded in BI’s reporting. The article says Klarna teams had discussed adding email-based OTP as an additional control, but worried that stronger authentication would impair merchant conversion; one internal estimate reportedly pointed to roughly $28.5 million per month of GMV risk from the extra friction. That framing matters. It suggests the company was not merely surprised by a novel edge case, but was actively weighing checkout efficiency against the possibility of unauthorized access to prior customers’ accounts. For a company positioning itself not merely as a BNPL button but as a broader consumer-finance platform, that is a control-philosophy problem, not just an isolated bug.

The attached Reddit screenshot sharpens that point because it appears to show the same failure mode in the wild before the later BI article: OTP login tied to a recycled number, exposure of another user’s personal information, and an allegation that a newly entered card could have been attached to the pre-existing account. On its own, that complaint is anecdotal and should be presented as such. In combination with BI’s later reporting, it supports a narrower and more defensible conclusion: recycled-phone-number risk was visible both publicly and internally, yet stronger controls appear to have been rolled out only after the issue became acute. Klarna says it has now fully rolled out email OTP and resolved the issue.

Klarna’s conduct suggests revenue protection outranked consumer protection.

Business Insider’s coverage suggests Klarna treated the login-control issue as a commercial trade-off before it treated it as a trust issue. Internal messages focused on conversion drag, merchant sensitivity, and partner fallout, even as staff acknowledged uncertainty around the true scale of recycled-number cases and the possibility of meaningful remediation and legal cost. Only after the issue became acute did the company authorize a broader patch and begin framing the response for merchants, regulators, and consumers.

Business Insider article link: https://www.businessinsider.com/klarna-data-leak-exposed-customer-logins-2025-11

Cross-Cutting Themes and What Would Change Our Mind

A coherent bearish case emerges when the above issues are read together.

Narrative versus economic substance. The Moritz purchase is not, in isolation, a thesis. The eBay AOV claim is not, in isolation, a thesis. Stripe distribution is not, in isolation, a thesis. Together, they form a pattern: Klarna’s external story increasingly depends on signals—confidence signals, partner “impact” signals, distribution “scale” signals. Skeptics ask the same question in three domains: what remains after the signal decays?

Merchant-adoption optics versus activation reality. Klarna’s disclosures concede that MoR channels provide a substantial portion of merchant revenue and that it intends to keep driving growth through them. That increases the burden on management to provide activation and concentration data, not just merchant totals.

Promotion mechanics in partner metrics. The eBay coupon is a textbook example of a tiered incentive structure that can inflate AOV. Investors should assume similar structures exist elsewhere unless management clearly discloses otherwise.

Earnings quality and the capital markets. A company that leans heavily on adjusted measures and receivables offloading must expect a higher discount rate until the model produces durable, GAAP/IFRS-consistent profitability through cycles.

What would change our mind is straightforward—and measurable:

· Stripe channel transparency: disclosed activation cohorts that separate “enabled” merchants from merchants with meaningful GMV, broken out by partner (Stripe vs direct vs other PSPs), with churn and GMV-per‑merchant trends.

· eBay normalization evidence: a disclosure (or third‑party corroboration) showing the “~3×” AOV persists outside the June 2–6 coupon window and is not dominated by threshold bunching near the coupon tiers.

· Earnings durability proof: a multi‑quarter demonstration that statutory profitability follows the non‑IFRS narrative, without relying on unusually favorable asset‑sale pricing.

· Governance and disclosure discipline: fewer “mechanics coaching” moments and more forward‑looking disclosure that anticipates the market’s real questions before volatility forces reactive clarification.

Downside-Oriented Valuation Framework

A defensible downside framework begins with a simple premise: in credit‑sensitive fintech, the market does not pay for GMV; it pays for credible, cycle‑resistant earnings power.

Public disclosures for FY2025 highlight $3.5B of total revenue and $65M of adjusted operating profit (about 1.9% adjusted margin), alongside negative EPS for the year. Reporting around February 2026 describes a sharp drawdown and a market value around $5.3B after the stock drop, implying the market is already discounting meaningful risk.

From here, the downside debate is about whether Klarna’s “banking expansion + AI efficiency” narrative translates into sustainable margin, or whether the business is in a prolonged state of (i) mix‑driven provisioning drag and (ii) funding/asset‑sale dependence.

A conservative activist short framework uses scenarios tied directly to the issues above:

Scenario A: “Normalization haircut” (moderate downside).

Assume revenue growth persists but “impact” metrics are discounted as partially promotion‑ or channel‑driven (eBay‑style), and merchant growth is re‑interpreted as enablement rather than high‑velocity activation (Stripe‑style). In that scenario, the multiple paid on revenue compresses because the market comes to view growth as lower quality and less defensible. This scenario does not require a credit blow‑up—only a credibility and durability repricing.

Scenario B: “Margin mirage” (deep downside).

Assume that the combination of higher‑duration credit mix and funding/forward‑flow pricing makes the “deferred profitability” story persist longer than expected, keeping statutory profitability elusive. In that world, valuation converges toward a low multiple of revenue (or a book‑value‑like framework if the market begins treating the company as a bank‑risk hybrid without bank‑grade disclosure). The catalyst is not necessarily a recession; it can be a widening of spreads in asset sales or a step‑up in realized losses.

Scenario C: “Channel renegotiation / partner friction” (idiosyncratic downside).

If a “substantial portion” of merchant revenue is sourced through MoR channels like Stripe/Adyen, then any adverse renegotiation or change in placement/terms can pressure take rate and volume. This is fundamentally a bargaining‑power and concentration risk—one that can show up as slow, silent margin erosion rather than a discrete blow‑up. The market tends to under‑price these risks until a partner change is announced.

We emphasize what this framework is not: it is not a claim that Klarna’s business is fictional. It is a claim that the market should price Klarna as a credit‑intermediating, partner‑dependent platform until empirical results prove otherwise—and that, in such businesses, multiples can compress quickly when the story is revealed to be promotion‑assisted.

Questions for Management and the Board

Moritz / Crankstart buy, promotion, and governance protocols:

- What internal trading‑window, blackout, and pre‑clearance policies governed the March 3–11 chair‑linked purchases—particularly given the proximity to the March 9 lock‑up expiration and the company’s March 6 “mechanics” release?

- Why did the company choose to publicize the lock‑up “conversion mechanics” in the level of detail provided? Who initiated the disclosure, and was the board consulted?

- Was the board (or a committee) informed in advance of the chair’s intention to purchase through an associated entity/Crankstart‑linked vehicle? If so, what recusal or information‑barrier procedures were applied?

- Does Klarna view the chair’s purchase as purely philanthropic/long‑term in nature, or as a market signaling mechanism? Why was it disseminated via a press release rather than simply through the Form 3 disclosure?

- How does management plan to operate under the new Section 16(a) reporting regime applicable to foreign private issuers after March 18, 2026 (including monitoring of 10b5‑1 plans and Form 144 activity)?

eBay partnership economics, the “~3×” claim, and promotion mechanics:

- For the eBay “~3× AOV” statistic: what period does it cover (the full quarter vs a subset after launch vs a promotion window), and what is the sample definition (all Klarna transactions, first‑time Klarna users only, etc.)?

- How much of the Q2 2025 AOV uplift is attributable to the June 2–6 tiered coupon program requiring Klarna as sole payment method? Did you observe threshold bunching near $150/$250/$550?

- Please quantify: (i) eBay‑funded discount dollars during the coupon period, (ii) incremental GMV attributable to the promotion, and (iii) post‑promotion retention (repeat rate) of Klarna‑activated eBay buyers.

- When quoting eBay’s “impact” language in your earnings materials, why was the contemporaneous, eBay‑funded coupon not disclosed as key context?

Stripe partnership, merchant adoption quality, and IPO-window optics:

- Of the merchants counted in your total merchant number, what percentage are (a) “enabled” through Stripe vs (b) actively processing meaningful GMV through Klarna? Please provide: active‑merchant definitions, channel splits, and churn rates.

- In Q1 2025, you reported 724,000 merchants and “150,000 new retail partners.” Define “retail partners,” reconcile it to “merchants,” and quantify gross adds vs churn.

- What portion of merchant revenue is derived through MoR channels (Stripe/Adyen) versus direct relationships? What is the sensitivity of take rate and margins to changes in these platform relationships?

- To what extent did Stripe‑enabled “instant” availability materially affect merchant metrics and narrative in the lead‑up to the September 2025 IPO? Provide a pre‑IPO and post‑IPO merchant activation waterfall by channel.

- Did Klarna’s board or audit committee evaluate whether the Stripe relationship implicated related-party disclosure or approval standards given Sequoia’s >10% stakes in both Klarna and Stripe, Michael Moritz’s historic board-level roles across both ecosystems, and Sequoia’s current representation on both boards; if so, what was the conclusion, who made it, and what facts supported the view that the IPO-window expansion of Stripe and Klarna’s arrangement was negotiated and maintained on fully arm’s-length terms?

Earnings quality, receivables sales, and credit/funding sensitivity:

- Provide a bridge that decomposes transaction margin dollars into (i) core run‑rate margin and (ii) the contribution (or drag) from receivables sales/offloading (gains/losses), with sensitivity to forward‑flow pricing.

- What proportion of your consumer credit exposure is retained vs sold, by product and geography, and how do you reconcile cohort performance when exposures are transferred off balance sheet?

- How should investors think about statutory profitability versus adjusted profitability over a full credit cycle, particularly as longer‑duration products scale?

Cybersecurity:

- When did senior management and the board first become aware that recycled phone numbers could allow access to prior customers’ Klarna accounts, and how many substantiated complaints or support tickets were logged before the November 2025 remediation?

- What analysis supported delaying or limiting stronger authentication measures such as email OTP, and how did Klarna weigh the reported conversion and GMV impact against consumer-harm, legal, and regulatory risk?

- How many accounts were actually affected, what data fields were exposed, how many consumers and merchants were notified, and what criteria will Klarna use in deciding whether further regulatory disclosures are required?

Disclosure

This report reflects our opinions and research, which we believe to be accurate. We encourage readers to consider the sources cited and to conduct their own due diligence. This report does not constitute financial advice or an investment recommendation. We have no business relationship with Klarna. Our aim is to highlight our concerns and advocate for management to provide answers that will benefit all market participants in understanding Klarna’s business better.

Citations

· “Klarna Group Plc clarifies mechanics of March 9 lock-up expiration” (Investor Relations press release), Klarna, Mar. 6, 2026.

· Form 3 (Initial Statement of Beneficial Ownership) for Michael J. Moritz (Klarna Group plc), SEC EDGAR, filed Mar. 12, 2026 (purchase window Mar. 3–11; 3,472,845 shares; $49.9M consideration; held through Crankstart Foundation).

· “Klarna Board Chair Michael Moritz Acquires 3.47 Million Shares for $50 Million” (press release), Klarna Investor Relations / Business Wire syndication, Mar. 13, 2026.

· “HFIA Act … final rules” (press release), U.S. Securities and Exchange Commission, Feb. 27, 2026.

· “Holding Foreign Insiders Accountable Act Disclosure” (Final Rule release PDF), SEC, Feb. 27, 2026 (effective date March 18, 2026; Section 16(a) applicability).

· “HFIA Act Frequently Asked Questions” (Corp Fin guidance), SEC, Mar. 2026 (Form 3 timing guidance for FPIs).

· “TEAM” page listing founders (Harriet Heyman and Michael Moritz), Crankstart, accessed Mar. 2026.

· “eBay x Klarna Tiered Coupon | eBay.com” (official coupon terms; tier thresholds; funded by eBay; June 2–6, 2025), eBay, accessed via eBay coupon page.

· “Q2’25 Results – Financial Services Solutions Driving Growth” (slide stating AOV on Klarna transactions ~3× U.S. marketplace average), eBay earnings presentation PDF, Jul. 30, 2025.

· “Second Quarter 2025 Results” (press release; partnership expansion to U.S.; repeats eBay quote including ~3× AOV), Klarna Investor Relations earnings release PDF, Q2 2025.

· “eBay Inc. Reports Second Quarter 2025 Results” (press release; notes deepened partnership with Klarna and expanded BNPL access across U.S.), eBay Investor Relations, Jul. 30, 2025.

· “Klarna is now available to millions of new businesses … strengthened partnership with Stripe” (press release; 25 countries; doubled new merchants in Q4 2024), Klarna, Jan. 14, 2025.

· “Klarna accelerates global momentum in Q1 2025 …” (press release; 724,000 merchants; 150,000 new retail partners; Stripe integration), Klarna, May 19, 2025.

· “Klarna Group plc – Form 20-F for FY ended Dec. 31, 2025” (risk disclosures on MoRs; naming Adyen/Stripe; reliance on partner banks/service providers; revenue composition excerpts), Klarna, filed Feb. 26, 2026 (PDF as hosted on IR).

· “Klarna Announces Pricing of its Initial Public Offering” (pricing; NYSE ticker KLAR), Klarna press release, Sept. 9, 2025.

· “Klarna Completes Initial Public Offering” (closing; $40 IPO price; shares began trading Sept. 10; mix of primary vs. selling shareholder shares), Klarna Investor Relations / Business Wire syndication, Sept. 11, 2025.

· “Q4-25 Klarna Group plc Earnings Release” (non-IFRS measures; transaction margin dollars; receivables offload/gain/loss framing), Klarna Investor Relations, Feb. 19, 2026.

· “Q4 2025 Earnings Press Release” (headline metrics; quarterly highlights), Klarna Investor Relations, Feb. 19, 2026.

· “Klarna Group plc Publishes Full Year 2025 Results” (FY2025 summary figures; adjusted operating profit; negative EPS), Klarna Investor Relations, Feb. 26, 2026.

· “Klarna stock sinks 27% after bad loan costs soar” (market reaction; contextual reporting on provisions/losses), Financial Times, Feb. 2026.

Source Links

· https://www.sec.gov/Archives/edgar/data/2003292/000120104526000001/xslF345X02/primary_doc.xml

· https://pages.ebay.com/coupon/2025/fsi/klarnaus/

· https://www.businessinsider.com/klarna-data-leak-exposed-customer-logins-2025-11

· https://s205.q4cdn.com/644747736/files/doc_financials/2025/q4/Klarna-Group-plc-20-F-2025.pdf

· https://www.ft.com/content/dbe5de32-1274-4adc-9e14-c05823ca9d76

· https://www.klarna.com/international/press/klarna-announces-pricing-of-its-initial-public-offering/

· https://investors.klarna.com/financials/quarterly-results/

· https://www.reddit.com/r/PersonalFinanceCanada/comments/1lustn7/klarna_is_very_insecure_and_leaks_your_information/