Figma (NASDAQ: FIG) – From Design Darling to Investor Beware

Author’s Note: We are short Figma stock (via long put options) and stand to benefit if its share price declines. All information presented here is derived from public records and sources, which are cited in brackets. We invite readers to review these sources and form their own conclusions.

(I) Key Findings (Overview)

Overhyped IPO, Troubled History: Figma – a collaborative design software firm – rode a wave of hype through a July 2025 IPO after a failed $20B acquisition by Adobe. Its stock initially tripled (briefly valuing Figma near ~$70B)[BI], but we believe this enthusiasm ignored serious internal issues and an inflated valuation not supported by peers or fundamentals.

Importantly, Adobe’s stock plunged ~17% on the Figma deal announcement[Creative Boost] and rose when the deal was scrapped[Investopedia] – a clear market signal that Figma was overvalued and/or problematic. After announcing the Figma deal in September 2022, Adobe’s 1-day drop represented ~$29.5B of market cap destruction – indicating public shareholders valued Figma at negative ~$9.5B. Adobe stock continued lower in the weeks that followed.

After the Adobe deal was terminated, Figma did several private financings in 2024 at $10B and then $12.5B sequentially[Reuters]. The first of these was a January 2024 opportunity for employees to liquidate shares at a $10B valuation (a paltry ~$9B enterprise value after removing the $1B Adobe break fee cash was infused just a month earlier). This was dilutive to junior employee stakes, while concentrating ownership for both Figma’s non-selling, top executives and VC investors purchasing shares in the round.

Undisclosed Security Breach: Evidence from X (Twitter) and Reddit indicates Figma’s sales team exploited an internal tool to access private customer file names – essentially peeking into users’ work – in order to pressure them into upgrades. This occurred as late as Oct 2025, months after Figma claimed to have “fixed” a similar privacy lapse[Reddit]. Other customers report they had identical issues months or years earlier. Figma never disclosed this incident to investors or the public, despite SEC rules requiring prompt reporting of material cybersecurity breaches[Harvard Law]. When we raised concern to Figma Investor Relations, the company’s General Counsel responded and indicated plans to conduct only a cursory internal inquiry focused on an individual bad acting sale’s representative. However, CEO Dylan Field quietly acknowledged the cybersecurity issue to a few clients and social media followers—without alerting Figma’s broader user base, market participants, or regulators.

Egregious Sales Misconduct: We uncovered a pattern of aggressive and deceptive sales practices at Figma. Customers report relentless high-pressure tactics: account reps tricking admins into “support” calls that turn into pitches, contacting finance departments behind admins’ backs to upsell, weaponizing their own platform’s security as a sales “scare tactic”, auto-charging for “hidden” seat upgrades that users never explicitly approved, duplicate seat charges for the same user, and surprise “true-up” bills that come too late. These are not one-offs – systemic abuse is corroborated by numerous user accounts, suggesting a toxic sales culture prioritizing short-term revenue over ethics[Reddit6][Reddit7].

Pre-IPO Financial Gimmicks: In the lead-up to its IPO, Figma pulled multiple levers to inflate its growth metrics. It synchronized the timing of aggressive promotions like free FigJam whiteboard seats and “Dev Mode” trials that later converted to paid plans, delayed the release of “Connected Projects” that would eliminate Figma’s double-charging of freelancer and agency seats, and in March 2025 implemented a hefty 20–35% price hike across core subscriptions[Pricing SaaS]. These moves temporarily boosted Net Dollar Retention (NDR), ARR growth, and revenue. We estimate Figma’s true NDR (excluding one-time boosts, dark patterns, and using a full customer cohort) is well below the IPO’s 132% headline – likely around 105-110% – once normalized for these tricks and dark patterns. Further, after shifting its NDR methodology during the IPO process, the company did not restate past NDR or clearly flag the material change to NDR methodology (e.g. early IPO S-1 excluded customers who fully-churned or down sells below $10k ARR)[SaaS.WTF], leaving investors with at best a confusing picture of this non-GAAP metric and at worst an overly rosy reported figure.

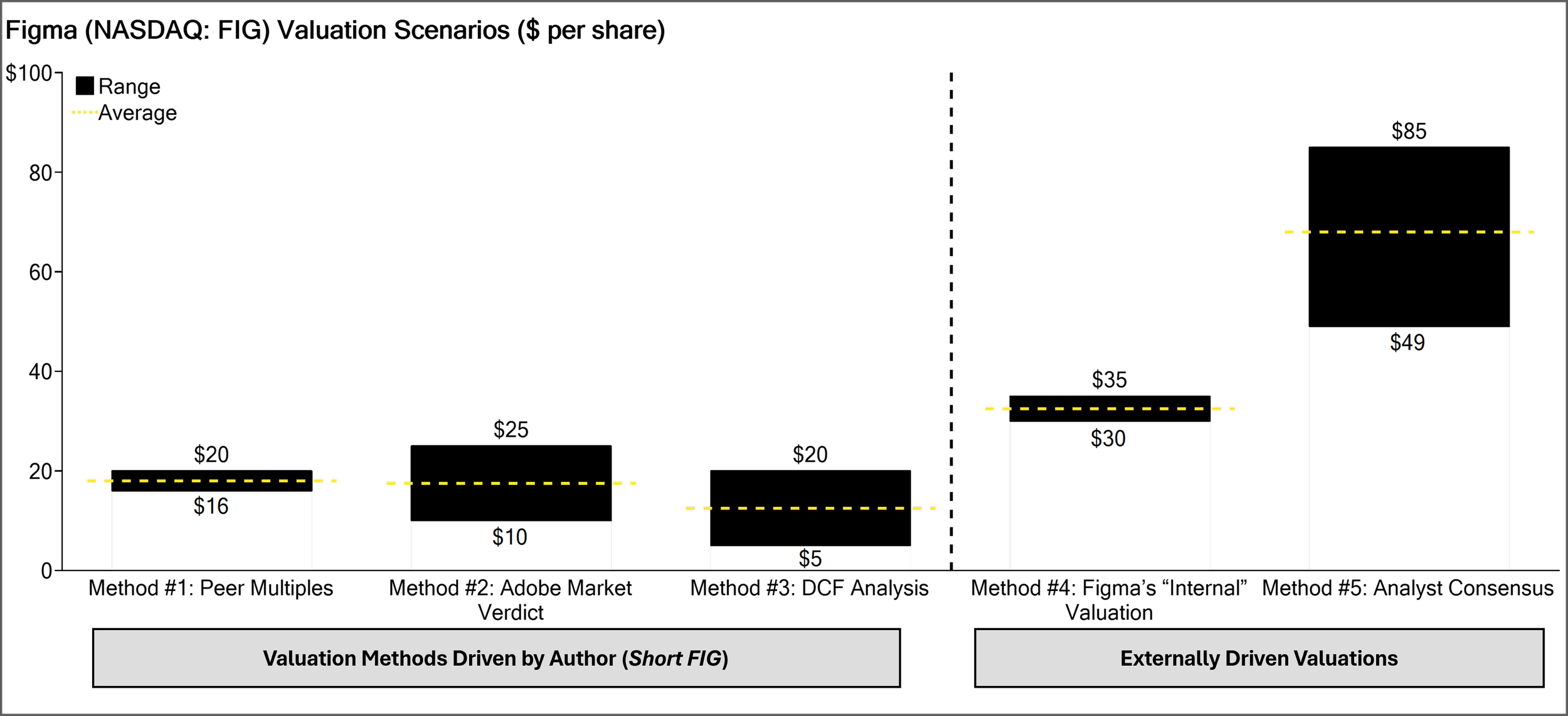

Sky-High Valuation & Downside Risk: Even after cooling from its peak, Figma continues to trade at an extreme revenue multiple versus SaaS peers. Its adjusted growth and retention metrics are solid but not unique, and its current valuation prices in years of flawless execution – just as customer dissatisfaction is beginning to snowball. Meanwhile, share lockup overhang looms, with insiders and VCs holding the majority of shares (Index Ventures alone owns ~13%[BI]) – many likely eager to cash out post-lockup. We argue that informed investors (as evidenced by Adobe’s share price reaction) assigned Figma low or even negative real value. Our DCF analysis (see “Valuation Concerns”) indicates significant downside potential for FIG shares. In short, we see Figma as a highly overvalued company propped up by transient pandemic-era success, short-term levers and pull-forward via marketing and price increases, questionable marketing practices, unethical upsell tactics, and opaque or missing financial disclosures. As post-IPO lockup expirations approach, we believe Figma should face increased public market scrutiny.

In the sections below, we detail each of these findings with evidence and analysis.

Figma shares have fallen ~76% from its post IPO peak. (As of: November 4, 2025 | Sourced via: Bloomberg Terminal)

(II) Overview of Figma’s Business and Failed Adobe Deal

What is Figma? Figma is a cloud-based design and prototyping platform that allows teams to collaborate on user interface and product designs in real time. Founded in 2012 by Dylan Field (then a Thiel Fellow) and Evan Wallace, Figma launched to the public in 2016 and quickly gained traction among designers for its browser-based, multiplayer approach to design work[BI]. Over the next decade, Figma raised approximately $333 million in venture funding from top Silicon Valley firms, attaining a $10B valuation by 2021[Reuters]. By May 2024 – after over a year of deal limbo with Adobe ended with Figma receiving a $1B termination fee from Adobe – Figma was first valued at $10B in January 2024 (implying a $9B enterprise value when excluding the $1B cash break fee from Adobe) and then $12.5B (enterprise value of $11.5B net of the $1B break fee) in a May 2024 tender offer – with both rounds allowing employees to cash out shares[Reuters][Reuters].

Adobe’s attempted acquisition: In September 2022, Adobe (NASDAQ: ADBE) shocked the tech world by announcing plans to acquire Figma for $20 billion in a cash-and-stock deal. The offer (roughly 50× Figma’s then-annual revenue) was seen as staggeringly high, and Adobe’s own investors immediately registered their disapproval – Adobe’s stock plummeted on the news[Creative Boost], erasing nearly ~$30B in Adobe’s market cap in a single trading session on September 15, 2022 (far more than Figma’s purchase price—implying a negative value for Figma).

Over the next year, global regulators scrutinized the deal on antitrust grounds, with the EU and UK raising concerns that merging Figma with Adobe would stifle competition[Blog][Blog]. Facing this opposition, Adobe and Figma abandoned the merger in December 2023, with Adobe paying a hefty $1B termination fee to Figma as a breakup penalty[Investopedia][Investopedia]. Adobe’s stock climbed ~1.8% on the official; announcement that the $20B Figma deal was off and had been creeping higher on rumors the deal might get terminated[Investopedia]. In other words, Adobe shareholders celebrated being unable to buy Figma at $20B and were even happy to pay the unusually high $1B (5% of deal value) break fee – a telling indication that informed observers viewed Figma as wildly overpriced and value-destructive at $20B.

Freed from the deal (and flush with a billion-dollar termination windfall), Figma forged ahead on its own. The company launched four new products in 2024 (including a whiteboard tool FigJam, a developer handoff mode, “Figma Slides” for presentations, and other features) – moves that some investors framed as a positive outcome of the failed merger[BI]. By early 2025, Figma boasted strong headline financials: $228M in Q1 2025 revenue (up 46% YoY) and even a quarterly profit of ~$45M[Reuters][Reuters], a rarity for a growth-focused SaaS firm even after pulling out Bitcoin from the PnL. Figma’s customer base had reportedly grown to ~450,000 paying customers (teams and individuals) by 2025, including over 1,000 enterprise customers with $100k+ in annual spend[Blog][Blog] – an enviable roster featuring the likes of Netflix, Stripe, Duolingo**, and more. However, aspects of Figma’s IPO growth story were fueled via short-term levers that at a minimum are unlikely to be repeated and arguably are eroding Figma’s reputation and position in the marketplace.

Note: **Figma’s S-1 highlighted Duolingo as a customer while a Figma lead director (John Lilly) also sat on Duolingo’s board, and Figma added Duolingo’s CEO (Luis von Ahn) to Figma’s board about a week before its IPO. It likely didn’t require separate disclosure, but the Duolingo callout is worth contextualizing: clearly, Figma and Duolingo have close ties.

Summer 2025 IPO: On July 28, 2025, Figma priced its IPO on the NYSE under ticker “FIG”. Initially targeting a ~$18.8B valuation—raising ~$1.2B with the majority of that amount (around $789 million) going to selling shareholders versus the balance of ~$411M going to the company[Reuters][Reuters]. Strong IPO demand led Figma to boost the offer price to $33/share – above the marketed range[BI]. The stock exploded ~250% on its debut, opening at ~$85 and closing around ~$115[BI][BI]. This exuberant debut briefly valued Figma near ~$70B – almost 3.5× the price Adobe was willing to pay just two years prior[BI]. Such a pop in a long-dormant IPO market made Figma the poster child of a “hot” tech listing, and early investors enjoyed a windfall—at least on paper.

However, since that peak, reality has been setting in. As of this writing, FIG trades around $50 – still well above its $33 IPO price, but far below the frenzied first-day levels. Even at ~$50/share (≈$24.4B market cap), Figma carries a revenue multiple of ~27× trailing sales, an eye-watering valuation by any measure. For comparison, other high-growth, profitable SaaS companies typically trade at 10–15× sales or less in 2025’s market. The bull narrative is that Figma’s best-in-class net retention (132% NDR)[Blog] and ~40–50% recent growth could justify a premium. But as we show, those metrics have been propped up by one-time gimmicks, confusing reporting, and murky and aggressive sales tactics. As these serious concerns around Figma’s business practices and governance emerge – we raise the question of whether this “design unicorn” will stumble now that it’s under the public microscope.

In the sections that follow, we detail our findings on Figma’s undisclosed security breach, sales misconduct, manipulated metrics, and valuation, citing a variety of primary sources (SEC filings, user testimonies, industry analyses, etc.). We recommend that investors exercise extreme caution with FIG – we believe the stock’s downside is substantial.

(III) Undisclosed Cybersecurity Breach: Sales Reps Snooping in Customer Files

Our research uncovered a disturbing privacy breach that we believe Figma has not disclosed via appropriate channels: Figma’s sales representatives have been accessing private customer file metadata – including file names and/or project information via an internal “interface” to identify upsell opportunities, violating user trust, customer contracts, and potentially regulations. Even more troubling, this practice has persisted for 6+ months despite Figma claiming to have fixed the issue months ago.

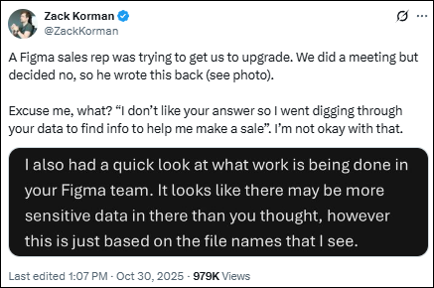

The “Pistachio” incident (Oct. 2025): On October 30, 2025, the CTO of a cybersecurity startup (“Pistachio”) went public on X (formerly Twitter) with an alarming allegation: a Figma sales rep, in the course of pushing an enterprise plan upgrade, reviewed the names of private design files in the company’s Figma account – without any permission or invitation. After Pistachio had declined to upgrade Figma plans, the rep effectively spied on the team’s Figma usage to gain leverage in the sales pitch (for example, mentioning specific file names to suggest the customer needed the upgraded Figma plan’s “enhanced” security features). We view the Figma Rep’s attempt to upsell a cybersecurity startup by leveraging its own cybersecurity breach as a deeply concerning and manipulative sales tactic—with a clear disregard to customer confidentiality all in the interest of Figma’s own pecuniary gain.

The Pistachio CTO, Zack Korman, blasted this “scare tactic” as a serious breach of trust and a violation of data privacy. (As a cybersecurity professional, one can imagine Mr. Korman’s horror that a vendor’s salesperson was snooping on his company’s internal projects.)

According to posts summarizing the incident on X, Mr. Korman’s public call-out prompted a scramble inside Figma: CEO Dylan Field privately reached out to the CTO to apologize.

On the same X thread, a separate Figma customer publicly reported that this same data-access issue occurred approximately six months ago—well before Figma’s IPO. This customer reported that the company had acknowledged the breach and represented that the access “was an oversight and shut down.” Mr. Korman’s post demonstrates that the practice continued. These customer complaints demonstrate that Figma knew of the unauthorized access before its IPO, failed to disclose it, and misled customers and investors by asserting that the issue was resolved (when it was not).

After learning of this serious cybersecurity incident and apparent lack of governance, we sent Figma’s investor relations a formal request to preserve documents and disclose the scope and internal awareness of a sales interface that reportedly allowed inappropriate access to customer file names, metadata, and potentially other information. Figma’s General Counsel, Brendan Mulligan Esquire, ostensibly launched an “investigation.” Mr. Mulligan, replied via email:

“We received your email… We are aware of the situation that you reported, and we are formally investigating the sales representative’s behavior. We are also reviewing our training and protocols. We will determine the appropriate response at the conclusion of that process.”

Mr. Mulligan’s description of Figma’s investigation appears notably narrow in scope—reportedly focusing on the individual sales representative’s conduct. This may be designed to allow the company to avoid any public disclosure or customer-wide cybersecurity breach notification, treating it as an internal matter resolved by a quick policy reminder or training to sales staff. To date, Figma has issued no 8-K, no blog post, no mention in its SEC filings about this incident. We have followed up with Mr. Mulligan to request a broader investigation:

"However, multiple customers have publicly reported identical experiences months apart—indicating the existence of a shared internal interface visible to sales staff that exposed confidential customer file names and metadata…

Notably, on October 30, 2025, CEO Dylan Field publicly acknowledged on X that Figma identified an internal sales-support “interface” that inadvertently allowed metadata visibility across accounts and described a customer phone call regarding the same. These admissions strongly suggest the problem was systemic, not isolated, and that multiple sales representatives had similar access over an extended period.

Accordingly, please confirm:

1. Has Figma determined whether the “sales interface” issue constitutes a material cybersecurity incident under Reg S-K Item 1.05 or Item 106?

2. If so, when was that determination made, and has a Form 8-K or other public disclosure been filed or prepared?

3. Has Figma’s Disclosure Committee or Audit Committee reviewed potential Reg FD implications of the CEO’s selective communications?"

Why this is material: Figma’s handling of the above incident is highly suspect. Under the SEC’s new cybersecurity disclosure rules (effective 2023), public companies must report material cybersecurity incidents within 4 business days of determining they are material[Harvard Law]. A sales team having backdoor access to customer workspaces – and using that access inappropriately – absolutely could be deemed material. Figma is a cloud software whose reputation hinges on data safety and user trust; an incident that undermines those could “reasonably impact” investors’ view of the company. On Mr. Korman’s viral X thread, customers report identical issues dating from at least 6 months ago. Additionally, numerous customers have expressed their outrage with some indicating they would be cancelling their Figma accounts and others indicating the cybersecurity breach would allow for contractual contract termination—all hallmarks of a material cybersecurity incident. In our view, the first report of this cybersecurity breach and internal “interface” should have been evaluated for S-1 disclosure—at least 6 months ago (before Figma’s IPO) according to customer social media posts. Instead, it appears Figma did not shutdown the interface after the first customer complaints—despite Figma claiming they had to the reporting customer. The narrow investigation described by Figma’s GC may again be attempting to quietly avoid proper disclosure of this ongoing cybersecurity incident.

Furthermore, if a salesperson could access file names, it implies broader internal access controls problems. It’s unclear how widespread this practice was and Figma seems eager to conduct a narrow investigation unlikely to uncover the truth. We asked ourselves: Was it an isolated rogue rep, or an allowed tactic encouraged from the top? We discovered serious reports on Reddit suggesting cybersecurity and controls issues going back to at least 2024, indicating it is far from isolated:

In mid-2024, a Figma user warned that sharing a prototype link could inadvertently expose all pages of a file to the viewer, calling it a massive privacy oversight. The user wrote: “Figma… made a change that bypasses the user’s privacy rights… prototypes you share give access to the entire document… just navigate to the core URL… voila, free access.”[Reddit][Reddit] This user explicitly called out Figma staff, saying “You are a GDPR call away for forcing users to leak their privacy and private data without their knowledge.”[Reddit][Reddit] In a Reddit discussion titled “Figma data leaks.”, others confirmed it “hasn’t been fixed” despite being known for years[Reddit].

In another thread, the user describes how an external party gained access to his confidential Figma project because a client accidentally shared a link. The OP laments that Figma’s settings make it too easy to leak data, and pleads: “that’s clearly bypassing user’s privacy rights… I urge stakeholders, including regulatory bodies and advocacy groups, to publicize this matter, investigate these practices and consider legal actions… The community deserves a platform that genuinely prioritizes safety over profit.”[Reddit] (This impassioned call to action underscores how betrayed some paying customers felt about Figma’s cavalier approach to data privacy.)

Customer complaint (Reddit): “Even now a person won’t notice it until someone starts playing with the prototype link you shared… [It’s] clearly bypassing user’s privacy rights… You are a GDPR call away from forcing users to leak their private data without their knowledge. And I bet there’s no compensation for any of these. I urge stakeholders, including regulatory bodies and advocacy groups, to publicize this matter, investigate these practices and consider legal actions… The community deserves a platform that genuinely prioritizes safety over profit.”[Reddit]

Notably, the Reddit user above mentions “They said previously they had taken steps… but obviously they haven’t”[Reddit] – indicating Figma was aware of the privacy issue and claimed to fix it, but the fix was either ineffective or incomplete. This aligns with what we see in the Pistachio case: Figma’s leadership knew about internal data access concerns (because users had flagged them 6+ months earlier), tried to paper over it without truly closing the loopholes, and got caught again.

Breach or “feature”? Whether one calls these incidents “breaches” or just “abuse of features,” the crux is the same: Figma’s internal systems allowed non-technical employees (sales reps) to view customer information that should have been private. At best, this is a glaring security design failure. At worst, it’s an intentional growth tactic (giving sales insight into customer usage patterns and projects to hit overly aggressive quotas around Figma’s IPO window) that management willfully turned a blind eye to. Neither scenario inspires confidence.

From an investor standpoint, the risk is twofold:

Reputational/operational risk if enterprise customers lose trust and churn away (no CIO wants a SaaS vendor whose reps peek at their IP), and

Regulatory risk if Figma is later forced to disclose these incidents or gets investigated/fined for not disclosing them. The SEC has recently charged companies for “misleading cybersecurity-related omissions”[Harvard Law].

The bottom-line:

Figma’s silence here could put shareholder value at risk.

Questions that arise: Why didn’t Figma proactively disclose this issue once discovered and reported to the company over 6 months ago? Did the company perform any legal/regulatory analysis of whether the file-access incident was material? If not, that’s a governance failure. If yes, and they concluded “not material,” we would strongly question that judgment. Also, what steps (if any) has Figma taken to prevent future sales snooping? The company’s help center and privacy policy make no mention of this scenario. Are file names and project titles considered “customer personal data” under Figma’s policies? If so, this could also run afoul of data protection laws (as the Redditor noted re: GDPR).

In summary, Figma appears to have concealed a significant security incident to avoid bad press ahead of its IPO and lockup expiration. This lack of transparency is a red flag. If management hid this, what else might they be hiding? We believe investors deserve full disclosure on this incident and any similar cases. (See our Questions for Management section at the end, where we specifically ask Figma to come clean on this matter. We have also emailed Figma’s GC asking the same.)

Select user posts on two X threads regarding the “Pistachio” incident (Oct. 2025):

Pistachio CTO (the Customer) Thread: https://x.com/ZackKorman/status/1983943961220690003

Figma CEO Dylan Fields Response: https://x.com/zoink/status/1984028464278860252

(IV) Egregious Sales Misconduct: “Dark Patterns” and High-Pressure Tactics

Figma’s problems aren’t limited to technical breaches – they extend to the very way the company makes its money. Our investigation found a widespread pattern of sales misconduct and customer abuse. It appears Figma’s push for growth at all costs has fostered a “win dirty” culture in its sales organization, leading to deceptive billing practices and harassment of customers. These claims are backed by numerous firsthand accounts on customer forums and social media from Figma’s paying clients (many posted in 2025 before and after Figma’s IPO). The sheer volume and consistency of complaints suggest the issues are systemic, not just a few bad actors.

Key abuses reported by customers include:

Fraudulently contacting unrelated departments to force upgrades: Multiple Figma admins recounted how their account managers, frustrated at being rebuffed by the usual point-of-contact, would go around them and reach out to higher-ups or other teams. In one egregious case, after an admin at a multinational firm declined to move to Figma’s expensive Organization plan, the Figma rep directly contacted the company’s finance department and claimed the team was “migrating to the Org plan,” effectively tricking finance into thinking an upgrade was already decided and approved[Reddit]. This caused internal confusion (“tech leaders, other admins… asking me what the rep was talking about”[Reddit]) and put inappropriate pressure on the original admin. The admin complained to Figma, asking that the rep be removed for “shady stuff.” Figma’s response? “Of course Figma didn’t do anything, and the rep is trying to contact other people inside our teams to sell the Org license.”[Reddit] Essentially condoning the rep’s behavior. This is highly unethical sales conduct, bordering on fraud (impersonating or falsely representing a client’s intentions).

Customer testimonial (Reddit): “Next thing I know, the rep goes and contacts our finance dept and tells them we’re migrating to the Org plan. You can imagine the stir… Finance, tech leaders, other admins, all asking me if I decided by myself… a real mess. I told Figma… asked them to remove the rep, since we have no interest to work with someone that does shady stuff. Of course Figma didn’t do anything, and the rep is trying to contact other people inside our teams to try and sell the Org license.”[Reddit][Reddit]

High-pressure meeting bait-and-switch: Figma reps have been reported to set up calls under false pretenses – e.g., offering help with a billing issue or a product demo – only to turn it into a surprise sales pitch. One small-business user shared: “Our account rep wasted my time under the guise of helping with an issue… then immediately launched into an upsell pitch for the Organization plan.”[Reddit][Reddit] The user felt “very icky” about the call and said the rep even asked to speak with other team members “who she thinks would benefit from the other plan”[Reddit]. This kind of bait-and-switch tactic erodes trust and is reminiscent of the worst “used-car salesman” stereotypes.

“Dark pattern” auto-billing of seats: Perhaps the most anger-inducing issue for customers has been Figma’s seat management system, which many describe as a “dark UX pattern” by design[Reddit]. Historically, if any user in your team requested edit access on a file (even mistakenly), Figma would automatically upgrade them to a paid Editor seat – instantly charging the account for an extra seat without any admin approval or even notification until a “true-up” bill would be sent weeks or months later. The admin only discovers the charge later on the invoice, often after accumulating months of fees. One user explained: “Any editor can just press ‘accept’ when another user requests edit rights and they are instantly upgraded to a full editor seat, without letting you or an admin know… You only notice after you get the bill.”[Reddit] Another concurred: “I’m convinced they do it this way on purpose to bleed you out for more paid seats.”[Reddit] This is classic “sneak into basket” behavior – a known deceptive practice where a system opts you into paying for something unless you proactively opt out (which Figma made impossible, since the upgrade was automatic).

None of this is new: Figma’s billing has long been engineered so that what looks like a harmless viewer can silently morph into a paid editor seat—with the bill showing up later. Prior to 2025, numerous admins reported that view‑only users could self‑upgrade to paid editor simply by taking an “upgrade action,” without any admin approval or notification—leading to surprise seat creep and surprise charges. (Reddit)

After public backlash, Figma changed the workflow in March 2025 and now touts admin approval. But the default is not what it seems: the Help Center says the new default is “Manually approve, unless seat is available.” If you’ve pre‑purchased seats, users can still be auto‑assigned into them—no approval click required. In short: the “fix” still contains a loophole that converts usage into billable seats by default. (help.figma.com)

Figma’s “fixes” may be inadequate. Even in environments explicitly set to “always needs admin approval,” customers have reported non‑admin users seeing approval prompts and being able to approve upgrades themselves—an alarming control failure that undermines the claimed guardrails. Separate threads explain that no email alert goes out when a seat is auto‑claimed from available inventory, leaving admins to discover the growth only when they audit settings—or when the invoice hits. (Reddit)

Shockingly, as of last month: Figma still defends the practice as evidenced by a “best answer” on Figma’s hosted customer forum. Figma’s support employee explains retroactive, prorated seat charges using a failed “restaurant” analogy. The reply frames post-usage invoicing as normal while omitting the crucial steps that at a restaurant customers are brought a menu and then asked what they would like to order. This is very basic customer consent.

Why this matters: Whether by design or “accident,” this funnel quietly increases paid seats and elevates expansion metrics. The behavior pre‑2025 looked like a textbook dark pattern; the 2025 “fix” keeps a silent auto‑assignment path open if “available” seats exist. In both variants, revenue expansion happens first, transparency second.

Difficult seat cancellation & phantom “unused” seats: Compounding the above, Figma made it extremely hard to remove or downgrade seats. Customers on annual plans cannot remove a user mid-term; you have to remember to do it in a narrow window before auto-renewal, or you’ll be charged for the entirety of the next year[Reddit]. Even converting an Editor seat to a cheaper “dev” seat didn’t truly downgrade – Figma would keep the full seat active (but “unused”) and bill you for both unless you contacted support to eliminate the old seat[Reddit]. These practices are so beyond the norm that seasoned admins likened Figma to the worst of legacy software vendors. “I have never seen any company that doesn’t allow you to cancel an automatic renewal – congrats, Figma,” one wrote, sarcastically[Reddit]. Another commented: “Seats are a big mess. Clearly it’s by intention… This is the s**t Adobe is hated for.”[Reddit][Reddit] Ironically, Figma – once seen as the fresh, user-friendly upstart alternative to Adobe – has embraced the very dark patterns that made Adobe reviled.

Misleading scare tactics: Users also reported that Figma reps attempted to scare them into upgrades using dubious claims. For example, multiple customers said their rep insisted that staying on the lower-tier “Professional” plan was a security risk, claiming “your current plan isn’t secure, you should be on Organization for security”[Reddit]. There is little technical basis for this; it appears to be a canned talking point to create FUD (fear, uncertainty, doubt) and push a more expensive tier. Customers saw through it (“pretty poor form”[Reddit]) especially when they heard the exact same line from different reps – “It’s like a bingo card in these comments at this point,” the original poster observed after hearing others got the same spiel[Reddit].

Billed twice for the same seat: On Figma’s community forum and Reddit, many freelancers and agencies have complained that Figma “charges me for every user who accesses my files, even if they’re already paid users”[Medium]. A frustrated agency owner described the situation plainly:

“I own an agency, and we have freelancers that already pay for their own license, but then I need to pay for an additional license for them when they’re on our project… We have clients that we collaborate with, and we either need to pay for them to have a seat on our account or they have to pay for us to have a seat on their account despite us already having seats of our own. I mean, it’s kind of genius that they’ve found a way to bill twice for the same seat, but it has really driven me to the point of trying to find alternatives.”[Reddit]

This “bill twice for the same seat” policy has understandably angered customers. Some have even questioned its legality under consumer protection rules. In the same Reddit thread, one user wrote that Figma “ha[s] to be breaking FTC rules by not even alerting people that by simply sharing a file with full edit access, you are going to be charged for a ‘seat’ for each person. It is absurd… not even just a dark pattern, it is full-blown intentional obfuscation.”[Reddit] Another commenter called it “the scammiest thing about Figma so far,” saying “they’ve found a way to bill twice for the same seat, which is an insane business model.”[Reddit] These candid reactions show the level of frustration: some users have floated the idea of a class-action lawsuit to stop the practice[Reddit].

From a legal standpoint, Figma’s approach likely toes the line of what is disclosed in the user agreement. The criticism is that admins often weren’t clearly warned in-app that inviting an existing Figma user with edit access would auto-upgrade (and bill) a new seat[Reddit]. Lack of upfront transparency could invite regulatory scrutiny (e.g. claims of unfair billing practices). So far, there’s no public record of an actual legal challenge, but the uproar pushed Figma to respond through product changes. The Connected Projects feature is essentially Figma self-correcting this issue before it further threatens customer goodwill, results in legal issues, or attracts regulators.

Surprise “True‑Up” Invoices / Revenue by Ambush: On Organization/Enterprise, Figma bills via quarterly “true‑ups” for seat changes between renewals. Figma’s own docs confirm that any seats approved between March 11 and your next renewal roll into your next true‑up / quarterly invoice. There’s a two‑week review window before Figma issues that invoice, but if admins miss it—or don’t know to look—the bill lands anyway (help.figma.com).

Real‑world complaints are consistent and recent:

May 1, 2025 (Q1 true‑up period): customers can’t reconcile “New charges since last invoice” even though the true‑up is owed—opaque accruals that appear only at true‑up. (forum.figma.com)

Historic and ongoing: admins say “quarterly true‑up needs to go away,” calling it ill‑suited for larger orgs; others report surprise charges and describe the system as “low‑key scammy” with dark patterns—forcing them to calendar reminders before invoices roll. (Reddit)

Figma Customer: “I ended up with over $1000 dollars in charges on a $12/month plan. I complained, they were willing to refund ONE month at $150. Then they double-billed me for $150 3 days apart. I am so mad. I trusted these people.” (Reddit)

Oct 10, 2025 (post‑Q3 close): invoice re‑issue requests and billing churn appear on Figma’s forum—another cluster right after quarter‑end. (forum.figma.com)

Figma says the true‑up model provides “flexibility”—upgrades take effect immediately, and the bill comes later. That’s exactly the problem: the cash registers ring first, and the human review happens (maybe) inside a short window before the quarterly invoice. The burden of vigilance is on customers; the benefit of ambiguity flows to Figma’s revenue line. (forum.figma.com)

Pattern to investors: True‑ups + auto‑assignment (if seats are “available”) = predictable seat creep and quarterly revenue lifts. Clusters of complaints line up around Q1 (Apr–May), Q2 (late Jun/early Jul), and Q3 (early Oct) 2025—precisely when true‑ups and renewals hit and, not coincidentally, during the IPO window. (forum.figma.com)

Collectively, these reports paint a picture of a company that is growth-obsessed to the point of abusing its users. The consistency across independent accounts is striking. On Reddit’s Figma discussion forum alone, we found dozens of firsthand posts in late 2025 detailing these issues, with titles like “Is this typical of your Figma account rep?” and “Dark patterns with everything involving seats”. We found the same on X and even Figma’s own community forums.

The consensus among customers/power users/admins:

Yes, it’s typical. Figma’s sales behavior is awful.

Additional illustrative quotes from paying customers:

“I blocked the rep that was contacting me because it was constant. Same issue.” (regarding relentless pressure to upgrade)[Reddit]

“They’re reusing the same (probably false) talking points… My rep said it’s unusual for an org like ours to be on a Professional plan… (which I suspect is totally bogus).”[Reddit]

“We share the same Figma account between countries… Figma rep said, ‘Figma doesn’t have a company your size using the professional plan.’… Next I know, the rep contacts our finance dept… (Figma did nothing when we complained.)”[Reddit][Reddit]

“Figma’s seat management is a really dark UX pattern… any user requests edit and gets upgraded, no admin knows… It does seem like a dark pattern driven by business goals rather than anything user-centered.”[Reddit][Reddit]

“They suck. The reps are useless. All they want to do is milk your company for money. The billing process is a giant pile of a and they purposefully make it obtuse so they can zap you for huge bills at ‘true up.’”[Reddit]

“It SUCKS that they’re the de facto tool. It’s going to be even worse now that they’re public and there’s higher pressure to sell… whatever tactics they use.” [Reddit]

It’s rare to see such a volume of negative feedback concentrated on a specific aspect (sales/billing) of a modern SaaS company. In our experience, this typically indicates the behavior is driven from the top – i.e., Figma’s management set aggressive targets and incentives that effectively encourage these tactics. It’s noteworthy that some comments speculate “now they’re public, pressure is higher”[Reddit], implying the environment worsened as Figma prepared for IPO (to pump metrics) and as a public company (to meet quarterly numbers). If true, investors should be alarmed: these short-term tactics burn customer goodwill and can lead to higher churn or backlash. In an industry as competitive as design software (with emerging alternatives like Penpot or even a revived Adobe XD—just look at XD’s iOS App Store reviews vs. Figma), Figma may be sowing the seeds of its own customer exodus.

Recent “fixes” – too late? Only after significant outcry did Figma finally make changes. In its March 2025 billing revamp (discussed in next section), Figma claims it “moved away from user-driven upgrades and given admins upfront approval over seat upgrades by default”[Figma Forum]. In other words, they acknowledge the old system was bad (“user-driven upgrades” = users auto-adding paid seats) and now admins have to approve seats. That’s a welcome change, but it raises questions: Why was such an obviously user-hostile system in place to begin with? (Hint: It was great for revenue, until people caught on.) And how many customers were quietly overcharged before this was fixed? Figma hasn’t apologized or refunded anyone as far as we can tell. The announcement of the fix was likely timed to prevent a backlash at IPO time rather than out of genuine empathy and users continue to report the same issues even within the last month.

From an investor perspective, the key point is that Figma’s growth has come, in part, through unsustainable means: squeezing customers with sneaky billing and bullying tactics. These behaviors can goose short-term expansion metrics (seats, ARPU, net retention), but they are not sustainable. Eventually customers rebel – as seen on Reddit and elsewhere – and some will leave. It’s notable that a number of users in those threads explicitly mention evaluating alternatives (“As soon as Penpot gets things we’re missing, it’s goodbye Figma”[Reddit], “Many are looking for other options,” etc.). If Figma’s NDR or growth were juiced by such tactics (which we believe they were), those numbers could decay quickly once the tactics are removed and frustrated customers continue to move elsewhere.

In summary, we see Figma’s sales conduct as a major risk factor. It indicates potential internal control issues (management either condoned unethical practices or negligently unaware – either is bad). It jeopardizes the long-term customer relationships that underpin any SaaS valuation. And it could draw regulatory scrutiny; deceptive billing and sales practices have, in other industries, led to FTC investigations, EU enforcement actions, or consumer protection lawsuits. Figma’s behavior might warrant such attention if it hasn’t already drawn it.

Investors should demand answers from Figma: How will you clean up your sales organization? What are the churn implications of these dark patterns? Do you risk a class action from customers over unauthorized charges? (We pose some of these in “Questions for Management”.) If the answer is dismissive or vague, that’s a big red flag.

Select user posts from Reddit below (use arrows to scroll):

(V) Pre-IPO Financial Maneuvers: Promotions, Price Hikes, and Smoke & Mirrors

Figma’s headline financial metrics – like its Net Dollar Retention (NDR) of 134/132% and robust revenue growth – have been a cornerstone of the bull case. However, our analysis indicates these figures were artificially inflated by a series of tactical maneuvers in the run-up to the IPO. By offering time-limited freebies and then converting them to paid, and by implementing across-the-board price increases right before going public, Figma created a one-time surge in expansion revenue that flatters its apparent customer retention and growth.

Let’s break down the key levers Figma pulled:

FigJam free, then paid: Figma launched FigJam (a collaborative whiteboard tool) in 2021 and made it free for at least its first year to drive adoption[Blog]. Starting in 2022, Figma began charging for FigJam for teams that wanted unlimited use, at $3–5 per user/month depending on plan[Blog]. This means many customers who were using FigJam for free in 2021 (and weren’t contributing to revenue) suddenly became paying customers for FigJam in 2022—boosting 2022’s ARR, NDR, and revenue growth around the 2022 Adobe deal negotiations. That conversion would register as “expansion” (increasing NDR) even though it was largely a result of a policy change (ending a free trial) rather than organic growth. After the Adobe deals termination in 2023, Figma once again used a freebie to boost FigJam adoption. This time, Figma ran a one-time Jamboard migration promo that gave up to 12 months of FigJam Professional free for teams that imported a Jamboard file and started an annual FigJam Pro subscription. It ended January 31, 2024 when unpaid FigJam users became paying customers. Thus, by 2024, FigJam had become a meaningful add-on offering and had plenty of users who had never paid for it—boosting 2024’s ARR, NDR, and revenue growth ahead of its IPO year. Then, right before the IPO, Figma decided to bundle FigJam into paid plans (no more separate fee) but correspondingly raised the core pricing (we’ll get to that later). The net effect: FigJam’s introduction, promotions, and monetization timeline gave Figma’s financials a one-time lift in 2022 and again in 2024. Then its later bundling helped justify a massive price hike in 2025 and establish Figma’s high “80% of customers use two products” metric that is really just an outcome of Figma’s new plans.

“Dev Mode” giveaway: In mid-2023, Figma announced Dev Mode, a set of features for developers to inspect designs and extract code. They introduced a cheaper “Dev Seat” for developers, priced lower than a full editor seat[Blog]. Initially, Figma allowed many customers to try Dev Mode for free or included it in existing editor seats (essentially a freemium approach to seed usage)[Blog][Blog]. By early 2024, they started monetizing it: customers could buy Dev seats separately, and later Figma would include Dev seats in the Professional (SMB) tier as well[Blog][Blog]. In 2025, with the pricing overhaul, Figma bundled Dev Mode access into the new seat structure – meaning many devs who had been using it for free now needed a paid Dev seat (at ~$12–15/month on annual vs monthly)[Blog][Blog]. This transition from free beta to paid feature likely drove an expansion wave: companies that gave Dev Mode a try in 2023 faced bills in 2024–25—driving IPO window revenue growth, NDR expansion, and ARR.

Figma Slides free trial: Figma’s foray into presentations, Figma Slides, launched in 2024. Like FigJam, Figma Slides was offered free for the rest of 2024[Blog], with plans to charge in 2025 ($3–5 per user, matching FigJam’s pricing)[Blog][Blog]. So during 2024, customers may have started using Slides at no cost (increasing their dependence on the platform). Then in Q1 2025, Figma signaled that Slides would become a paid add-on going forward. However, instead of charging separately and making the pricing page more complex, Figma again chose to bundle – as part of the March 2025 pricing change, Slides was included “for free” in all seat types[Figma Forum][Figma Forum] (Collab, Dev, Full seats all include Slides by default[Blog]). Of course, nothing is truly free: this bundling was part of the rationale to raise the core seat prices significantly and further supports the idea that Figma’s multi-product adoption metrics are not particularly insightful.

March 2025 price hikes (“Pricing 3.0”): This is the big one. Effective March 11, 2025, Figma rolled out a new pricing model that did a few things at once:

Consolidated seat types: They went from a mishmash of Editor/Viewer, plus separate add-on fees for FigJam/Slides, to three main seat tiers – Full, Dev, and Collab – each with defined access levels[Blog].

Included more in each seat: As noted, every paid seat now comes with FigJam and Slides capabilities (no separate add-on fee)[Figma Forum][Figma Forum].

Additionally, Figma’s 2Q2025 quarterly earnings press release prominently reported multi-product adoption as a triumph. In the report and earnings call, there was no mention that Figma’s new pricing model creates high multi-product adoption by default.

Raised prices significantly: The cost of a Full (editor) seat jumped ~20–35% (varies by plan; e.g. Pro plan from $15 to $20, Org from $45 to $55 monthly per editor, etc.)[Blog]. Collab seats (for non-designers) and Dev seats were introduced at new price points (Dev ~$12/mo annual). In effect, most existing customers saw a double-digit percent increase in their Figma bill once their renewal hit after Mar ‘25[Blog].

For example, the Professional (Team) plan editor seat went from ~$12/seat/month (annual) to $16 (annual) – a 33% hike[Blog][Blog]. Organization plan editors went from $50 to $60/user/month (approx, based on annual pricing) – a 20% hike[Blog]. Enterprise saw similar ~20% up. These are substantial increases, especially given Figma had already monetized new products from 2022–2024. The company messaged it as adding more value (free FigJam/Slides included)[Figma Forum][Figma Forum], but the reality is this was a monetary up-sell across the entire customer base.

The consequence of all the above: Figma’s Net Dollar Retention was — and continues to be — goosed by one-off changes rather than purely by organic growth or adoption. If a customer spent $100k on Figma in 2024, and in 2025 Figma jacked up prices 25% while the customer’s organic growth added 10% seat volume, that customer might now spend ~$138k – appearing as 138% NDR (great!) even if they only expanded their team usage by ~10%. It’s basically front-loading ~10-years of inflation in to the IPO-window, not sustainable expansion.

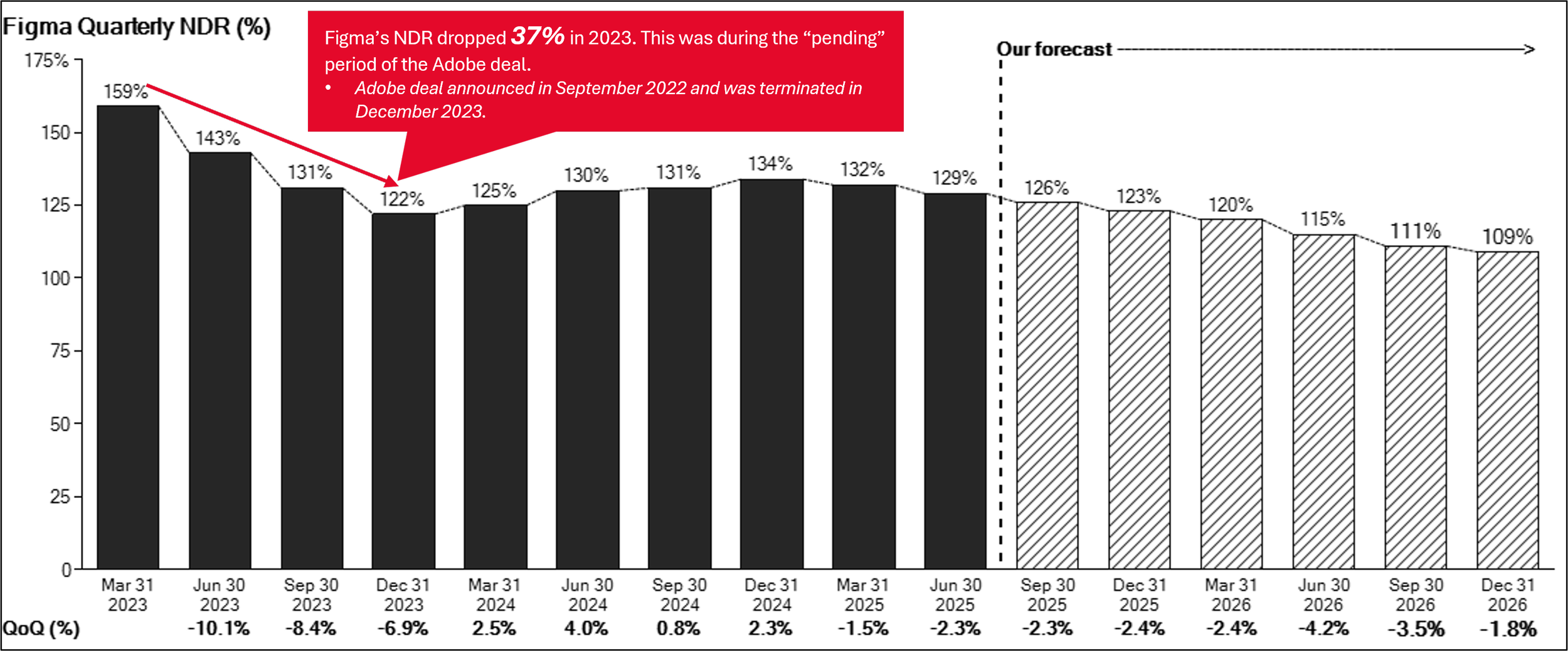

Figma is familiar with short-term boosts: There is evidence that Figma’s growth metrics surged before the Adobe acquisition was announced, only to dip during the prolonged merger review – a pattern that we believe is repeating around Figma’s IPO and early earnings results. Notably, Figma’s net dollar retention rate (NDR) – a key measure of revenue expansion within the existing customer base – spiked to an unusually high ~150% around 2022 (at the time Adobe’s $20 billion bid was made) and then plunged to roughly the mid-120s by the end of 2023[wing.vc]. In the same interval, Figma’s annual revenue growth decelerated sharply, from ~100% year-over-year during 2022 to only about 40% in 2023[wing.vc]. This post-acquisition-announcement slowdown suggests that Figma may have pulled forward a lot of expansion and upsells in 2022, boosting short-term results in anticipation of (or to justify) the Adobe deal, after which growth normalized at a lower level. Indeed, by late 2023 Figma’s fundamentals no longer looked as lofty as when Adobe first struck the deal – net retention fell, growth cooled, and the tech market’s multiples had compressed – making that rich $20 billion price appear increasingly hard to justify[wing.vc][wing.vc]. Officially, the merger was abandoned due to “no clear path” for regulatory approval[Reuters], but this steep drop in Figma’s momentum (clearly visible in its key financial metrics) during the 15-month antitrust limbo was surely a contributing factor in sapping enthusiasm for the transaction. See NDR table below regarding Figma’s steep 37% decline in NDR during the “pending” period of the Adobe deal (Figma’s NDR bottomed right in December 2023 when the merger was terminated).

Fast-forward to 2024–2025, and Figma seems to be employing similar tactics to “juice” its metrics in the run-up to its IPO. Some of these tactics are perfectly legitimate one-time boosts (e.g., price hikes) and we’re simply calling attention to the fact they will result in increasingly hard comps in the future. Figma’s short-termism regarding its egregious sales tactics (described earlier) is both more concerning for long-term investors and much harder to measure.

Let’s quantify the impact on NDR:

Another Analyst already did so we’ll share that: Figma reported 134% NDR for FY2024, and 132% as of Q1 2025[SEC] – world-class numbers. But fine print reveals this is calculated only on customers >$10k ARR and who remained >$10k ARR[Blog][Blog]. This biases the metric upward by excluding churn and downsells from smaller clients, as well as any big client that dropped below $10k. According to an independent analysis, Figma’s >$10k cohort (about 11k customers, just 2.5% of total count) contributed 132% NDR and made up 64% of ARR[Blog][Blog]. The remaining ~98% of customers presumably had far lower retention (some likely <100%). When the analyst modeled a plausible scenario for the whole base, they estimated blended NDR around 115–120%[9]. So immediately, the real retention is perhaps ~15 percentage points lower than the headline suggests, just by considering SMB churn.

Note: We notified General Counsel Brendan Mulligan of the apparent inconsistency in Figma’s Net Dollar Retention methodology the analyst above adjusted for. Figma’s S-1/A (May 23, 2025) defined NDR using a “dual-gate” >$10k ARR screen in both periods, which would exclude churned or downsized customers. The subsequent final S-1 and June 30, 2025 10-Q adopts a more standard cohort approach that includes expansion, contraction, and churn. Given Figma did not restate disclosed NRR figures of 134% (12/31/24) and 132% (3/31/25) from the May 23, 2025 S-1/A to its final version, we requested three clarifications (noting that clear disclosure of KPI methodology changes is required under Reg S-K Item 303(b)(3) and SEC Release No. 33-10751):

Whether the 12/31/24 and 3/31/25 NDR were calculated on a prior-period cohort including churn/shrinkage, or on a survivors-only basis.

If survivors-only, what the recalculated NDR/NRR would be under the 10-Q cohort method.

Whether any variance was deemed “immaterial,” and the quantitative analysis supporting that conclusion.

Ignoring NDR calculation methodologies, we still see considerable downside: As of 2Q2025, Figma reported its NDR at 129%—seemingly healthy. Importantly: 129% NDR is not a steady-state, quality metric – it’s been juiced. Out future steady-state NDR forecast makes the following adjustments:

STARTING NDR: 129% (As reported in Figma’s 2Q25 Form 10-Q)

LESS: Price Hike: 7.5% (2Q25 Earnings Call, Figma CFO: The one-time price hike contributed mid-to-high single digit %)

LESS: Dev Mode: 2.5% (EAQ Figma Financial Model)

LESS: Connected Projects: 1.0% (EAQ Figma Financial Model)

LESS: Sales Misconduct: 5.0% (EAQ Figma Financial Model)

LESS: IPO Window Promos: 1.0% (EAQ Figma Financial Model)

LESS: Size Penalty (Scale): 3.0% (EAQ Figma Financial Model)

ADJUSTED NDR: 109% (Author’s future “steady-state” forecast)

We expect it will take until the second half of 2026 for Figma’s NDR to reach our forecast — with downside should Figma face more severe penalties for their cybersecurity issues and egregious sales misconduct.

Quarterly NDR is as reported for the quarter’s ending March 31, 2023 to June 30, 2025. Future quarters use the author’s forecast.

Sources: Figma’s Form S-1 and Figma’s Form 10-Q (2Q2025)

(VI) Web Architecture Risks at Figma

Figma’s web‑first architecture delivers real‑time collaboration, but it also bakes in ceilings on performance, offline reliability, color management, openness of the file format, and “design‑to‑code” fidelity. Those ceilings matter more as files, teams, and—importantly—automation ambitions scale.

We’ve reviewed Evan Wallace’s website: https://madebyevan.com/figma/how-figmas-multiplayer-technology-works/.

Remember: Mr. Wallace is Figma’s technical co-founder and former CTO who left the company in ~2021 for “undisclosed” reasons.

How Figma actually works:

Rendering and core engine. Figma draws the canvas with a custom GPU renderer built on WebGL; the high‑performance editor core is written in C++ and bridged to a TypeScript/React UI. The early stack used asm.js and later WebAssembly to cut app load time by ~3×. This bypasses the browser’s DOM/SVG renderers to ensure cross‑browser fidelity.

Real‑time “multiplayer” sync. Clients speak to a document process over WebSockets; the system keeps a local copy, sends deltas, tolerates disconnections, and reapplies offline edits when you reconnect. Figma intentionally avoided OTs in favor of a simpler custom scheme; the company later moved critical server hot paths from TypeScript to Rust for latency and parallelism.

Plugins and sandboxing. Third‑party code runs in a VM sandbox (QuickJS compiled to WebAssembly) after Figma deprecated the Realms shim due to disclosed escape vulnerabilities in 2019. Plugins can read/modify the open file and call any external server; orgs can whitelist plugins. This is powerful, but it is also a data‑exfiltration vector if governance is weak.

File format and API. The on‑disk “Save local copy…” produces a

.figsnapshot that bundles schema and data; internally Figma serializes with a compact binary format (“kiwi”). The public surface for files is the REST API, which is rate‑limited and costed per endpoint. Heavy access will hit 429s and timeouts.

Product ceilings that show up at scale:

Figma failed the Moby Dick test, ran out of memory after freezing for 55-seconds.

Link: https://bjango.com/articles/designtoolmemory/

Memory and large‑file performance

Browser/Electron constraints show up under heavy documents. Independent testing finds Figma’s per‑document memory footprint materially higher than peers and prone to freeze or exhaust memory under text‑heavy stress tests; the author attributes part of this to per‑tab limits. Even if you accept that analysis cautiously, the direction of effect is clear. Bjango

In testing Figma’s memory capacity as of late 2023 (vs. competitors), the researcher wrote: “The idea is simple — create a text box and paste the entire contents of Moby Dick into it. Then, duplicate the text box and test memory usage with 5, 10, and 15 copies. Moby Dick is around 1.3 MB. It’s a hefty chunk of text, but by no means huge, especially for modern computers. Graph showing how much memory is used with multiple copies of Moby Dick pasted into a document. Figma and Sketch not shown. Illustrator, Affinity Designer, and Photoshop all about the same. The graph above looks a little empty, because Sketch and Figma both had issues with Moby Dick. Sketch froze not long after pasting the text. Figma froze for 55 seconds after pasting, then ran out of memory. Testing both apps again with a 200 KB text file gave similar results. The other apps handled 15 copies of the full Moby Dick text. I didn’t test beyond that point. Note that the memory usage for each additional text box seems minimal, which is what you’d expect, given it’s just 1.3 MB of text.”

Practitioner guidance around “memory usage at 70–90%” and file sharding is widespread, which is consistent with the above. It is anecdotal, but common. Reddit+1

Risk: Teams with massive libraries, many variants, or image‑heavy boards will see nonlinear slowdowns and operational friction as memory headroom collapses. This is a structural effect of the runtime, not a simple bug. madebyevan.com

Offline is partial, not primary

Figma’s client keeps working offline and will reapply edits after reconnection, but the model is cloud‑first: initial loads, file discovery, and some flows depend on service availability. That fits their own description of syncing and reconnect behavior. madebyevan.com

Third‑party write‑ups reinforce the practical constraint: to work offline smoothly you typically must have authenticated and loaded the file/pages before the connection drops. Treat those as operational workarounds, not guarantees. Supercharge Design

Risk: Travel, VDI, or high‑latency environments still experience brittle edges compared with native, fully local tools.

Color management and print workflows remain limited

Figma’s canvas is effectively sRGB‑centric and not fully color‑managed for wide‑gamut workflows; CMYK export isn’t native. Print‑oriented teams rely on plugins or downstream conversion. This is a long‑standing limitation noted by color experts and plugin vendors. Bjango+1

PDF import isn’t natively supported; teams lean on community plugins to pull PDFs in as vectors or images. That is friction for brand and print back‑catalogs. anything.to.design

Risk: Brand, marketing, and packaging teams face extra steps and fidelity risks when bridging screen and print pipelines.

“Design‑to‑code” is still guidance, not ground truth

Figma’s Dev Mode exposes measurements and generated snippets, but Figma itself steers serious teams toward Code Connect, which replaces auto‑generated code with snippets drawn from your real component library. That is an admission that raw codegen isn’t trustworthy in production without mapping to your system. GitHub+1

Developer sentiment reflects this: useful for inspection, unreliable for copy‑paste implementation at scale. That’s qualitative, but consistent. Reddit

Risk: Handoff gains plateau unless you invest in Code Connect integration and governance; simple copy‑paste code promises remain aspirational.

Accessibility of prototypes is improving but uneven

Figma added a prototype screen‑reader path (beta) so assistive tech can read prototype content, but this is relatively new and not equivalent to shipping accessible HTML. Early reports and how‑to guides confirm capability and limitations. Medium+1

Risk: Teams that conflate accessible prototypes with accessible products risk false confidence without developer‑side a11y work.

Binary format and rate‑limited APIs hinder open exit

The

.figsnapshot is a proprietary container (zip with bundled schema) and the live system serializes to an internal binary (“kiwi”). The API is the sanctioned interface; it is rate‑limited and time‑boxed on heavy endpoints. Migration and large‑scale synchronization require careful batching and backoff strategies. madebyevan.com+1Risk: At enterprise scale, “take your data and leave” is not a single click. It is an engineering project gated by quotas.

Desktop ≠ native

The desktop apps are Electron shells around the web engine. That means Chromium’s process and memory behavior applies on desktop too. Expect parity with the browser experience, not native OS performance semantics. Wikipedia

Risk: You do not escape browser ceilings by “going desktop.”

Service reliability remains a dependency

Figma acknowledges incidents tied to upstream providers; recent public updates flagged AWS‑related degradation. Third‑party status aggregators also show recent disruptions, including for new AI features. The point isn’t unusual downtime; it’s that single‑vendor cloud dependency is intrinsic to the product. X (formerly Twitter)+1

Risk: When Figma or its cloud provider(s) has an incident, design, review, and handoff can stall org‑wide.

Recent AWS outage in October 2025 caused Figma outage:

New vectors from AI features

MCP server and “Make.” Figma is pushing an AI‑augmented flow where models access design context and even the code behind AI‑generated app prototypes (“Figma Make”), including remote IDE integrations. This expands capability, but also creates new surfaces to secure and govern. These updates are very recent and still evolving. The Verge+1

Third‑party ecosystems matter. A recent high‑severity RCE in a third‑party MCP integration (not Figma’s server) illustrates how quickly AI‑adjacent tooling can become a security liability if unvetted. TechRadar

Risk: AI‑driven productivity becomes AI‑driven blast radius unless enterprises lock down integrations and audit scopes.

Bottom line: Figma’s engineering is world‑class, but its web‑first design sets the boundaries: GPU canvas in a browser/Electron, custom CRDT‑style sync, a binary scene format, and plugin/AI ecosystems that trade control for reach. At small scale this is a feature. At enterprise scale it is also a risk register: memory ceilings, partial offline, print/color gaps, codegen that requires mapping, proprietary snapshots, and cloud dependency. None of this is controversial if you read Figma’s own engineering notes. It is just physics.

(VII) Implications of Figma’s Low Float and Extended Lock-Ups on Stock Performance

(1) Insider/VC Ownership and Float Dynamics

Figma’s shareholder base is dominated by insiders and venture capital (VC) backers. As of Q3 2025, insiders (founders, executives, employees) held about 50.5% of the shares, and institutional investors (including VCs) held roughly 50.2%[Trading News]. This left only a tiny public float – at IPO in July 2025 Figma floated just 36.9 million shares (~6% of the company)[SEC FI]. Such a small float created artificial scarcity, meaning very few shares were available for trading initially. The immediate result was a frenzied IPO pop: priced at $33, Figma opened around $85 and closed its first day at $115.50 (a 250% jump from the IPO price)[SEC FI][SEC FI]. This explosive debut repriced the remaining 94% of shares (still held by insiders/VCs) at a much higher valuation without those holders selling any stock. In other words, a low-float IPO can benefit existing owners on paper by quickly boosting the value of their locked shares[SEC FI].

Such large insider and VC ownership implies that most shares are initially locked up, which drastically limits supply in the market. This often leads to high volatility and overshooting prices in early trading[Blog][Investing]. With Figma, the combination of huge demand ( reportedly 30× oversubscribed book) and scarce float created a classic supply-demand imbalance that sent the stock vertical[SEC FI]. In essence, heavy insider/VC ownership means public investors are trading only a sliver of total shares, so any buying or selling has an outsized impact on price. This scenario can keep valuations lofty in the short term, since insiders/VCs (who might be eager sellers) aren’t yet free to sell. It’s a double-edged sword: scarcity can drive big rallies, but if fundamentals don’t justify the valuation, a sharp correction can follow once more shares enter the float.

(2) Float % and Lock-Ups – Figma vs. Other Tech IPOs

Figma’s ~6% IPO float is exceptionally low, even among recent tech IPOs that have trended toward smaller floats. For comparison:

Instacart (Maplebear) – floated < 8% of shares in its 2023 IPO[6], resulting in a strong debut (+12% day-one). Executives explicitly chose a low float to provide liquidity mainly for employees, not to raise a ton of new capital[Investing]. This small float strategy created a supply/demand imbalance at first, similar to Figma.

Arm Holdings – floated ~9.3% of shares in 2023[Investing] (SoftBank retained the rest), and its stock jumped about +25% above IPO price on day one[8]. Arm’s tiny float (for a ~$50B company) made it prone to volatility – indeed, its shares pulled back over the next couple days[Investing].

VinFast (VFS) – an extreme case: only 0.3% of shares floated after its 2023 SPAC listing[Investing]. The result was a 255% surge shortly after debut (akin to a meme-stock frenzy)[8]. However, such moves often reverse – VinFast’s stock later collapsed to roughly half its peak value once initial euphoria passed[Investing].

These examples show Figma is not alone in using a “low float” IPO strategy. In fact, average IPO floats have been shrinking – in 2021 and 2022 the average float was ~18–19%, the lowest in decades according to IPO researcher Jay Ritter[Investing]. Figma’s ~6% float was far below that average, even among large tech listings. Low floats often produce big first-day pops and positive headlines (e.g. “stock doubles on debut”), as seen with Figma (158%+ pop intraday[Reuters]) and others. But a small float does not guarantee lasting gains – it can also “exacerbate losses if the share price drops” later on[Investing]. In essence, low-float IPOs amplify volatility in both directions. Once the initial hype fades, stocks like Figma can correct sharply – Figma indeed went from a high of ~$120 down to ~$50 in just a couple months[Trading News] as reality caught up with the hype.

It’s also worth noting that Figma’s IPO was intentionally structured this way. By selling only a tiny portion at $33, Figma left money on the table (the stock’s immediate surge implied the IPO was underpriced)[SEC FI][SEC FI]. Some criticized this as a $2–3B “gift” to IPO buyers, but others argue it was a strategic move – the enormous pop created buzz and “repriced” Figma’s remaining shares at a much higher valuation[SEC FI]. In other words, the VCs and insiders didn’t get all their cash upfront, but they now hold stock valued at ~$50 instead of $33. This strategy – using a small float to engineer a big pop – has been seen in other IPOs to signal confidence and generate momentum in a tepid IPO market[SEC FI]. The key takeaway is that Figma’s float vs lock-up mix was unusually skewed, even compared to similar large tech IPOs, and history shows such cases often have initial outperformance followed by volatile normalization.

(3) Short Interest, Borrowing Costs, and Low Supply

One immediate implication of Figma’s low float is a constraint on short selling. With so few shares freely trading, it’s very difficult for bearish investors to borrow shares to short the stock. Our own trades were constrained by this: we were unable to borrow shares—leaving long puts as the next best exposure. As of this writing virtually zero shares are available to borrow in the securities lending market, and any sporadic availability comes at a hefty borrow fee (recently ~20% annualized on Interactive Brokers)[Blog]. This double-digit borrow rate (which at times exceeded 20%+) reflects intense demand to short Figma combined with limited lendable supply of shares. Such high fees create a significant cost of carry for short sellers – a 20% annual borrow fee can eat away at any eventual profits, and it signals how scarce and coveted borrowable shares are. Figma’s short interest surged rapidly in the months after IPO: by mid-September 2025, short interest jumped to over 10 million shares (up 57% from late August)[Source]. As of the latest data in October, about 11.6 million shares were sold short, which amounts to ~26.6% of the public float being shorted[Source][Source] (over a quarter of all tradeable shares!). This is an enormously high percentage of float – for context, that’s on par with heavily shorted “squeeze” stocks. It underscores that many investors are betting on Figma’s richly valued stock to fall – but they face the hurdle of finding shares to short and paying high borrow fees for an extended period.

Historically, IPOs with tiny floats often see elevated borrow costs and short interest – and sometimes legendary short squeezes. For example, Lyft’s IPO in 2019 had such hard-to-borrow shares that initial borrow fees hit 100%+ annualized[Source]. Beyond Meat (BYND) in 2019 (and again last month!) is another case: with most shares locked up, BYND’s borrow fee averaged 70–90% early on (briefly over 100% for new borrows)[Source]. This made shorting extremely expensive and contributed to BYND’s stock skyrocketing ~8× above its IPO price before eventually crashing. Tilray (TLRY), the poster child of low-float mania, saw borrow fees soar to an insane 700% annualized ahead of its lock-up expiration, as only a tiny float traded while insiders were locked – shorts were effectively paying ~2% per day fee[Source]. These examples show that when 99% of shares are held by owners who can’t or won’t lend, shorting becomes costly or impossible[Source]. In Figma’s case, with ~90+% of shares held by insiders/VCs who likely aren’t lending shares, the short-selling capacity is severely constrained. This can prop up the stock price in the near term, since it limits one source of downward pressure (short sales) and can even lead to short squeezes if remaining float is aggressively bought.

However, the flip side is that high short interest on a small float also means any negative catalysts can trigger sharp drops as well – if some shorts have managed to position, even a small float increase or bit of bad news can send the price tumbling quickly when everyone rushes for exits. So far, though, short sellers in Figma have had modest influence. As one analysis noted in September, short interest was only ~2.5% of float at that time[Source] (float definition then was broader) and “limited pressure” from shorts was present – the real volatility driver was the lock-up expiration risk and lofty valuation, not shorts piling on[Source]. But that dynamic may change as more shares slowly enter the market (see next section) and as fundamental news comes out.

For a short seller, timing is critical in such situations. Entering too early means paying months of double-digit borrow fees while the stock’s float remains tight (which can keep the price higher than fundamentals merit). We’ve seen that short sellers often target the lock-up expiration as a catalyst for a price drop (since a wave of new supply can depress the price)[Source]. But they must survive until then. In Tilray’s case, many shorts actually covered just before the lockup release (to avoid the punitive 700% fees), which ironically caused a pre-lockup rally[Source]. Once the lock-up shares became available and borrow fees finally eased, Tilray’s stock did fall (–45% in the quarter after the lockup) and borrow cost normalized to ~20%[SP Global]. The lesson is that shorting a low-float IPO can be profitable in the long run, but it often involves painful carrying costs and volatility in the interim. In Figma’s case, the current borrow fee ~20%[Source] is lower than those extreme examples, but it’s still substantial – it will erode ~10% of a position (half of 20%) by next summer, for instance. And if any positive news or buying frenzy hits Figma while float is low, shorts could be forced to cover at a loss given the difficulty of maintaining the position. In summary, the scarcity of borrowable shares and high fees suggest that significant downside may not materialize immediately because short sellers are handcuffed in applying selling pressure until float increases and shares become available to borrow.

(4) Lock-Up Expiration Schedule and Delayed Selling Pressure

A crucial factor for Figma is its lock-up expiration calendar – essentially, when and how the currently locked shares (insiders’ and VCs’ holdings) can be sold. Typically, IPO lock-ups last 180 days (6 months), after which insiders/early investors can sell. For Figma, a standard 180-day period would have ended in late January 2026. However, Figma implemented a staggered lock-up plan:

Early Release for Employees: On September 5, 2025 (just ~5 weeks post-IPO), 25% of employees’ shares became eligible for sale because Figma’s stock met a performance trigger – it traded >25% above the IPO price for at least 5 consecutive days[Source][Source]. This early unlock was designed as a reward/liquidity for employees after the big stock surge. It added a bit of float (introducing some immediate supply). Indeed, around that time Figma’s stock dipped ~14% as this initial tranche hit the market amid broader growth concerns[Source][Source]. So we saw a taste of selling pressure when even a quarter of employee shares got unlocked.

Main IPO Lock-Up Expiry (Standard 180-day): Figma’s IPO prospectus indicated that the bulk of shares would be free to trade at the open of November 7, 2025 (this appears to be an accelerated timeline tied to the earnings schedule)[Source]. In fact, Figma announced that “substantially all” Class A shares under IPO lock-up would be released on Nov 7, 2025 per the original agreements[Source]. This would normally have unleashed a huge wave of stock into the market in November. However – Figma took an extra step to prevent a flood.

Extended Lock-Up for Key Holders: On August 30, 2025, Figma arranged an extended lock-up agreement with holders of approximately 54.1% of its Class A shares, restricting them from sale until August 31, 2026[Source]. In other words, over half the company’s shares (likely those held by major VC firms and possibly founders) agreed not to sell for a full year beyond the typical lock-up. This was a deliberate move to “stagger” the supply and avoid a sudden dump of shares in one go[Source]. Essentially, many of the largest pre-IPO investors voluntarily locked themselves up until summer 2026 to signal confidence and support the stock. Meanwhile, any shares not under that extended lock-up became free in Nov 2025 as scheduled. So after Nov 7, 2025, Figma’s float increases, but not by the full amount of insiders’ holdings – a huge chunk remains off-market until mid-2026.

This dual-layer lock-up strategy reflects a broader trend for hot tech IPOs to spread out unlocks and reduce immediate post-IPO selling pressure[Source]. Companies fear the classic pattern of stocks tanking at the 6-month mark when everyone rushes for the exit. By getting key stakeholders to agree to hold longer, Figma aimed to stabilize the stock in the interim[Source]. The trade-off is that the market knows a large supply overhang is still coming, just at a later date.

What does this mean for downside risk? In the near-to-medium term (late 2025 into early 2026), Figma’s float will remain relatively low. Even after November 2025’s lock-up termination, with the extended agreements in place the public float is only around 43.5 million shares out of ~410 million outstanding (≈10.6% float)[Source]. That’s still quite restricted. The biggest potential sellers – the VCs and large insiders – are essentially locked up until summer 2026, meaning they cannot add selling pressure until then. This artificially limits the supply of stock in the market for the next few quarters. With fewer shares available, it may indeed “limit the downside” in the stock for now, as the user suspected. Simply put, who is going to sell in size? Many early investors are contractually unable to until 2026. Those who can sell (employees, smaller holders) have partly done so or may trickle out sales over the winter. Moreover, with short sellers constrained by the factors discussed, there isn’t a huge pool of “synthetic” supply either. All this could mean Figma’s stock stays elevated longer than fundamentals alone would warrant, at least until the lock-up overhang starts lifting.

That said, low float doesn’t guarantee the stock can’t fall – it just changes the dynamics. The stock’s performance will still respond to earnings and sentiment. For instance, Figma dropped from ~$115 to ~$50 in the months after IPO even while most shares were locked, due to concerns about slowing growth and high valuation[Source][Source]. So negative fundamentals can drive downside even in low-float conditions – but possibly not as dramatically as if all holders were free to sell. Any current selling is mostly from new public investors adjusting positions or a trickle from early release shares, rather than massive VC liquidation. This could mean a somewhat grinding downward drift (as valuation moderates) rather than an immediate collapse. The real wave of selling pressure – and thus potentially the full bear case playing out – might indeed arrive only in mid-2026 when that 54% chunk of shares unlocks. At that point, some very large stakeholders (venture funds like Kleiner Perkins, Sequoia, etc., who got in at tiny valuations[Source][Source]) will have the first chance to realize gains. It’s reasonable to expect many will sell at least a portion of their holdings in summer 2026, simply as part of returning capital to investors or rebalancing. The supply shock from tens of millions of shares potentially hitting the market could put significant downward pressure on Figma’s stock – if the market hasn’t already priced that in. Often, savvy investors anticipate lock-up expirations: short interest tends to peak before the event and volume surges around the unlock date, with the stock sometimes sliding in advance[Source]. So by the second half of 2026, if it’s widely expected that “VCs will dump shares,” Figma’s price may weaken ahead of the lock-up expiration as traders position for it. Once the date arrives, if selling is as heavy as expected, the stock could decline further; alternatively, if the event was fully anticipated, the drop might be more muted or short-lived (sometimes stocks paradoxically bounce after a lockup expiration if the worst was already priced in before).